US oil stocks at their lowest since 2015

The weekly report from the US Department of Energy confirmed the current tightness in the oil market. US Crude oil inventories fell by 4.8mb last week and gasoline…

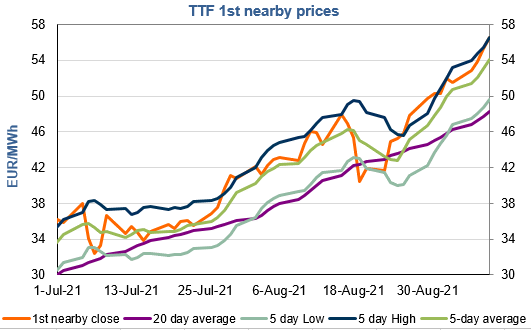

European gas prices extended gains yesterday, still supported by concerns on weak supply and low stock levels. Russian flows were slightly up, averaging 297 mm cm/day (compared to 296 mm cm/day on Wednesday), but still below the levels of end August (313 mm cm/day). As expected, Norwegian flows rebounded, to 284 mm cm/day on average, compared to 263 mm cm/day on Wednesday, as some planned maintenance works ended. The rise in Asia JKM prices (+1.56% on the spot, to €58.153/MWh) and in parity prices with coal for power generation provided additional upward pressure.

Moreover, comments from a Russian official saying that pumping commercial natural gas supplies via the Nord Stream 2 gas pipeline will not start until a German regulator gives the green light (a process which could last several months) did not help ease the bullish momentum.

At the close, NBP ICE October 2021 prices increased by 2.490 p/th day-on-day (+1.78%), to 142.150 p/th. TTF ICE October 2021 prices were up by 129 euro cents (+2.34%) at the close, to €56.581/MWh. On the far curve, TTF Cal 2022 prices were up by 82 euro cents (+2.22%), closing at €37.779/MWh, increasing the spread against the coal parity price (€35.399/MWh).

The market is waiting for clear signs of an increase in Russian flows in the coming weeks. For the moment, it does not see them and comes to the conclusion that Europe is obliged to enter into aggressive competition with Asia to attract LNG cargoes to replace the missing pipeline supply. Additional price increases are therefore likely for European gas prices. Only profit taking by financial participants and technical resistances (€57.515/MWh on TTF October 2021 and €37.739/MWh on TTF Cal 2022) seem able to calm the upward pressure.