US inflation rate hit a new 40-year high

The release of the US CPI figures showed a further acceleration in the inflation rate in March 2022 at 8.5% yoy, which was the largest year-on-year…

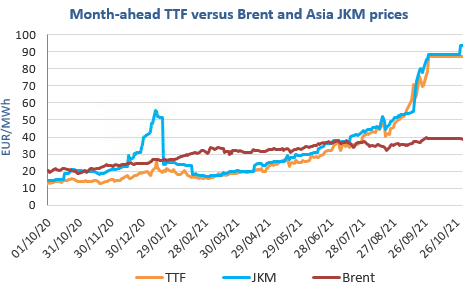

European gas prices increased strongly yesterday, still supported by supply concerns. Indeed, although Russian flows rebounded slightly yesterday, averaging 287 mm cm/day, compared to 280 mm cm/day on Tuesday, thanks to the slight rebound in Mallnow flows, they were significantly below the 315 mm cm/day of Monday. Norwegian flows were slightly down, to 337 mm cm/day on average, compared to 342 mm cm/day on Tuesday. On the LNG side, the additional rise in Asia JKM November 2021 prices (+2.99%, to €88.298/MWh), while spot prices weakened slightly to €93.241/MWh (-1.23%), means European buyers are obliged to continue to compete aggressively with their Asian counterparts to attract LNG cargoes.

Moreover, the rise in parity prices with coal for power generation (both coal and EUA prices were up) did not help calm the upward pressure.

At the close, NBP ICE October 2021 prices increased by 19.720 p/th day-on-day (+10.09%), to 215.100 p/th. TTF ICE October 2021 prices were up by €8.04 (+10.24%) at the close, to €86.609/MWh. On the far curve, TTF Cal 2022 prices were up by €3.42 (+7.00%), closing at €52.266/MWh, widening the spread against the coal parity price (€39.761/MWh, +2.33%).

Flows at Mallnow are nominated down this morning. This could continue to lend support to European gas prices today. The November 2021 contract on TTF ICE, the new 1st nearby from today, is currently trading at €91.675/MWh, chasing the Asian spot price, (€54.500/MWh for TTF ICE Cal 2022). The closing of the gap could temporarily calm the upward pressure.