Back in backwardation ?

Crude prices continued to be lifted by a declining US dollar, while the Libyan national oil company declared force majeure on its Hariga port due to budget…

European gas prices were mixed on Friday, torn between lower Norwegian supply, hopes of higher Russian flows and the additional easing in global coal markets. Norwegian flows dropped to 282 mm cm/day on average on Friday, compared to 301 mm cm/day on Thursday, still impacted by the unplanned outages at the Karsto gas processing plant and the Sleipner and Oseberg fields. Russian supply dropped slightly, averaging 276 mm cm/day, compared to 280 mm cm/day on Thursday. Note that statements by Russia saying that it will continue to meet its contractual gas supply obligations with its European customers helped to remove the risk premium on the Belarusian transit. Asia JKM prices (+5.42%, to €90.754/MWh, on the spot; +0.48%, to €94.065/MWh, for the December 2021 contract) and parity prices with coal for power generation (both coal and EUA prices were down) sent mixed signals.

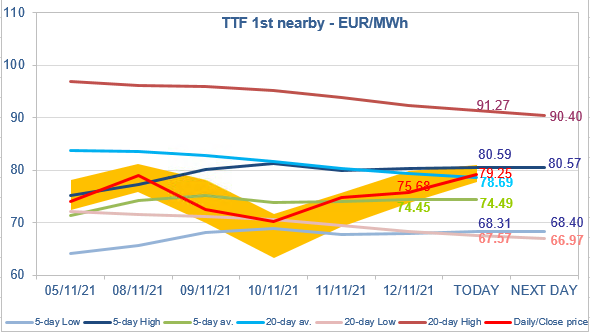

At the close, NBP ICE December 2021 prices increased by 0.720 p/th day-on-day (+0.37%), to 194.050 p/th. TTF ICE December 2021 prices were up by 88 euro cents (+1.18%) at the close, to €75.675/MWh. On the far curve, TTF Cal 2022 prices were up by 23 euro cents (+0.48%), closing at €48.167/MWh, and the spread against the coal parity price (€32.535/MWh, -1.51%) widened.

TTF ICE December 2021 prices traded in a narrow range on Friday between the 5-day average and the 5-day High. With Norwegian flows back to normal this morning (rising to 348 mm cm/day), the 5-day High should continue to set a resistance today. Only a major fundamental event could justify a break above this resistance level (which would open the door to a rise towards Asia JKM prices).