Macro & Oil Report: US economy: what we see and what we want to see

Macro & Oil Report: US economy: what we see and what we want to see Macro & Oil #105 In the latest EnergyScan podcast, Olivier…

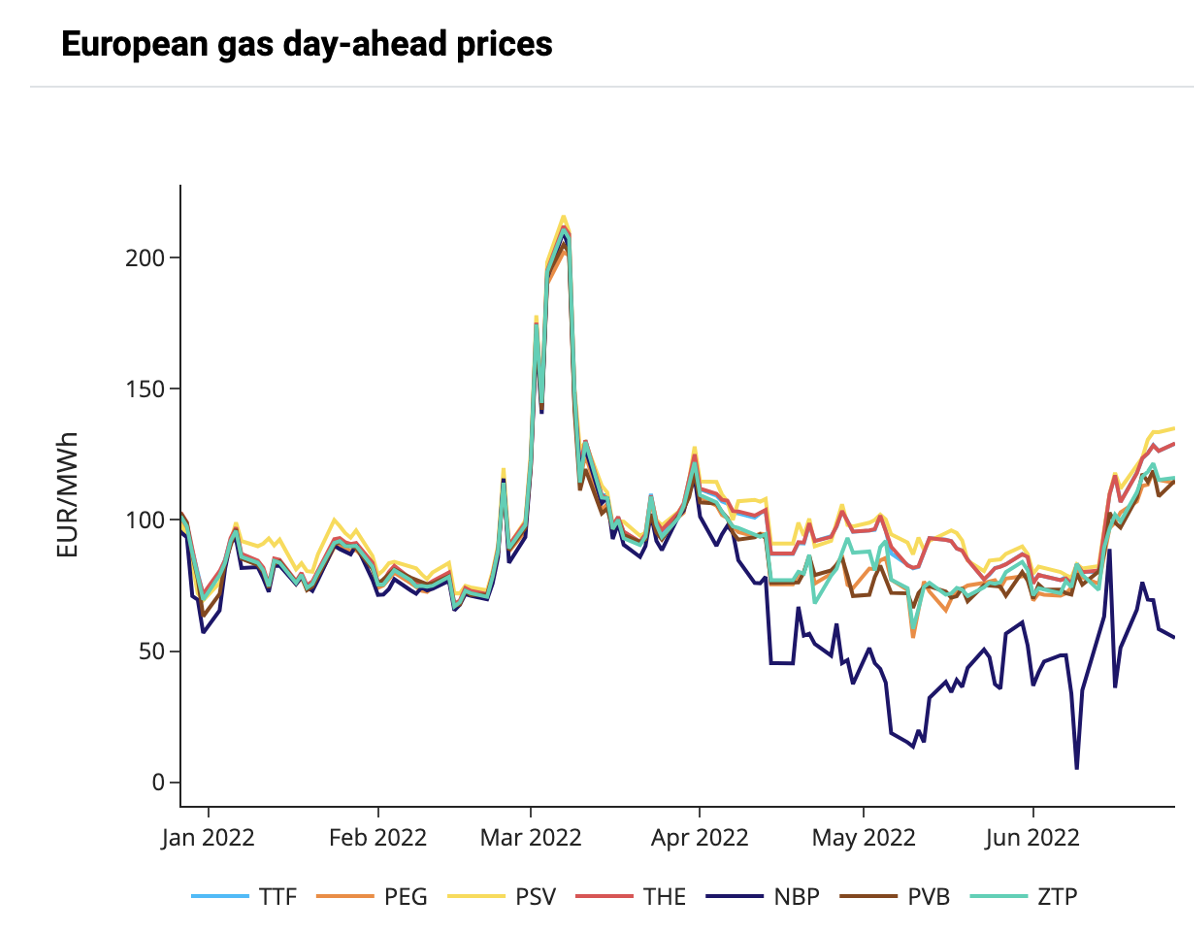

European gas prices were mixed yesterday, lacking support to climb much higher in a context of stable Russian flows and rebounding Norwegian flows (at 320 mm cm/day on average, compared to 311 mm cm/day on Friday). Day-ahead prices continued to trade in a wide range across European hubs, with NBP spot prices settling €75/MWh below German THE spot prices yesterday. Indeed, limited storage capacity and a large LNG import infrastructure in the UK are weighing on NBP spot prices while continental spot prices are trading at a much higher level on strong storage injection requirements and limited pipeline flows from Russia.

Note that following European Parliament approval on 23 June, the EU Council had definitively adopted the new rules on minimum gas storage obligations, which require member states to fill storage sites to at least 80% of capacity by 1 November this year, and to 90% by 1 November in subsequent years.

In terms of outlook for today on the supply side, Gazprom announced that Russian gas flows through the Turkstream pipeline resumed after a one-week maintenance. Note that Nordstream 1 annual maintenance will take place between July 11 and July 21. Other supply fundamentals remain largely unchanged with an unplanned outage at the Orman Lange field still constraining Norwegian exports by 13.4 mm cm/day. Prospects of rising wind speeds in Germany for next week could exert some bearish pressure on prompt contracts. Overall we favor a stable to slightly bearish outlook for European gas prices today.