Roller coaster

Financial markets continue to move in tandem with news from the Russian-Ukrainian border. At the end of last week, there was widespread pessimism ahead of…

Supported by higher demand, European spot gas prices increased yesterday, partially filling their discount against near curve prices. These latter were down overall, pressured by the drop in Asia JKM prices (-8.21%, to €103.963/MWh, on the spot; -0.09%, to €94.853/MWh, for the December 2021 contract). Far curve prices were more resilient, supported by the strong rise in parity prices with coal for power generation (thanks to the strong rebound in coal prices).

On the pipeline supply side, Russian supply was almost stable yesterday, averaging 265 mm cm/day, compared to 264 mm cm/day on Friday. Norwegian flows dropped to 343 mm cm/day on average, compared to 350 mm cm/day on Friday, due to a planned maintenance at the Gullfaks gas field.

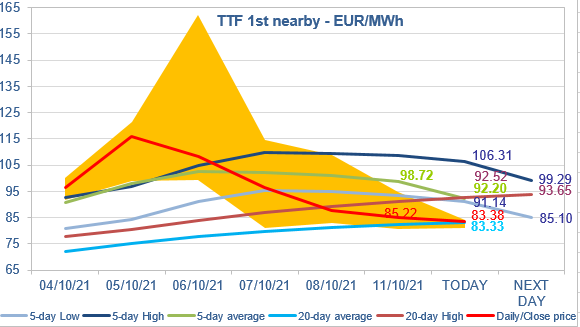

At the close, NBP ICE November 2021 prices dropped by 5.630 p/th day-on-day (-2.53%), to 216.580 p/th. TTF ICE November 2021 prices were down by €2.39 (-2.73%) at the close, to €85.216/MWh. On the far curve, TTF Cal 2022 prices were up by 21 euro cents (+0.42%), closing at €49.881/MWh, which reduced the spread against the coal parity price (€38.303/MWh, +5.91%).

Coal prices continued to rise in Asia today, which could continue to support gas far curve prices. As for TTF ICE November 2021 prices, they are slightly down this morning, but just like yesterday the 20-day average is lending support. Obviously, the market is still hesitant to break the uptrend. Given the many uncertainties (on Russian supply, on the power/coal/gas situation in Asia), it could decide to keep a wait-and-see position by trading between the 20-day average and the 20-day High.