European gas prices were mixed yesterday. Spot prices were slightly down, pressured by lower demand. By contrast, curve prices were rather up, more sensitive to the rise in oil and Asia JKM prices than to the drop in parity prices with coal for power generation (both EUA and coal prices were down). On the pipeline supply side, Russian flows were stable at 162 mm cm/day on average yesterday, as the Nord Stream 1 gas pipeline was still shut for the 10-day planned maintenance that started on 13 July. Norwegian flows were down, averaging 312 mm cm/day, compared to 320 mm cm/day on Wednesday.

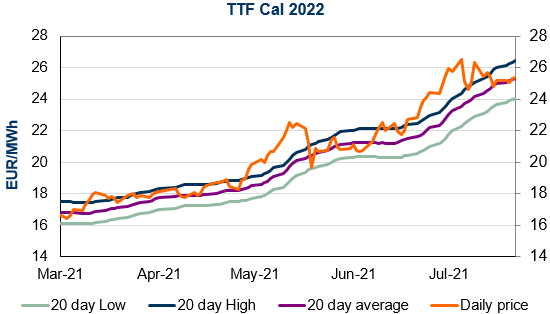

NBP ICE August 2021 prices were stable day-on-day, closing at 89.680 p/th. TTF ICE August 2021 prices were up by 18 euro cents (+0.50%) at the close, to €36.129/MWh. On the far curve, TTF Cal 2022 prices were up by 5 euro cents (+0.20%), closing at €25.352/MWh.

The restart of Nord Stream 1 could exert a downward pressure on European gas prices today. However, low stock levels and strong Asia JKM prices remain supportive and could contribute to limit losses. Moreover, technical supports (€35.800/MWh on TTF August 2021 and €25.250/MWh on TTF Cal 2022) could also trigger some buying.

The power spot prices slightly increased yesterday, supported by expectations of higher demand which offset the forecasts of improved French nuclear availability. The day-ahead prices…

The German elections have produced an even closer result than expected. The outcome of the forthcoming negotiations to form a government coalition looks very uncertain. The SPD…

Join EnergyScan

Get more analysis and data with our Premium subscription

European gas prices were mixed yesterday. Spot prices were slightly down, pressured by lower demand. By contrast, curve prices were rather up, more sensitive to the rise in oil and Asia JKM prices than to the drop in parity prices with coal for power generation (both EUA and coal prices were down). On the pipeline supply side, Russian flows were stable at 162 mm cm/day on average yesterday, as the Nord Stream 1 gas pipeline was still shut for the 10-day planned maintenance that started on 13 July. Norwegian flows were down, averaging 312 mm cm/day, compared to 320 mm cm/day on Wednesday.

NBP ICE August 2021 prices were stable day-on-day, closing at 89.680 p/th. TTF ICE August 2021 prices were up by 18 euro cents (+0.50%) at the close, to €36.129/MWh. On the far curve, TTF Cal 2022 prices were up by 5 euro cents (+0.20%), closing at €25.352/MWh.

The restart of Nord Stream 1 could exert a downward pressure on European gas prices today. However, low stock levels and strong Asia JKM prices remain supportive and could contribute to limit losses. Moreover, technical supports (€35.800/MWh on TTF August 2021 and €25.250/MWh on TTF Cal 2022) could also trigger some buying.