Prices down on improving stock levels

European gas prices weakened yesterday, pressured by improving spot fundamentals, as shown by storages that have switched to net injection mode for the European Union…

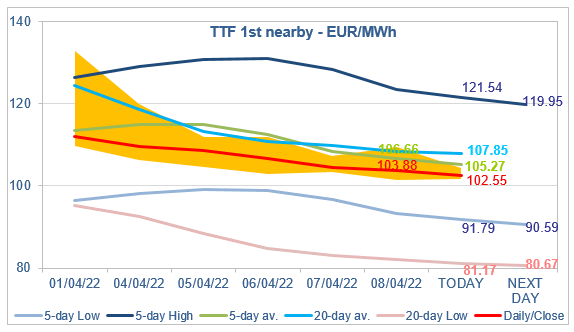

European gas prices were mixed on Friday, down overall on the spot (except in Italy) and the near curve, up on the far curve. The rise in Italy PSV day-ahead prices seems due to the fall in Russian flows, which averaged 241 mm cm/day in total, compared to 260 mm cm/day on Thursday. On their side, Norwegian flows increased to 320 mm cm/day on average, compared to 320 mm cm/day on Thursday. Far curve prices were supported by the strong rise in coal prices (+5.52% for API2 month-ahead prices, +5.74% for Cal 2023 prices) after the European Union formally adopted on Friday new sanctions against Russia, including bans on the import of coal (fully effective from the second week of August), wood, chemicals and other products which were estimated to slash at least 10% of total imports from Moscow. Japan, third-largest world importer after India and China, joined the movement and said it would ban coal imports from Russia.

At the close, NBP ICE May 2022 prices dropped by 4.950 p/th day-on-day (-2.12%), to 228.540 p/th. TTF ICE May 2022 prices were down by 68 euro cents (-0.65%), closing at €103.882/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.46 (+1.94%), closing at €76.358/MWh.

In Asia, JKM spot prices increased by 2.37%, to €99.225/MWh; May 2022 prices increased by 1.54%, to €105.430/MWh.

The rise in coal prices pulled the maximum coal switching level up to €93/MWh. But this failed to support TTF ICE May 2022 prices because they are trading much above this level and therefore continued their downtrend below the 20-day average. By contrast, TTF Cal 2023 prices on their side are trading very close to the maximum coal switching and were therefore more sensitive to their rise on Friday.

TTF ICE May 2022 prices are slightly weakening this morning. Given the levels of Asia JKM prices and the strength in coal prices, the downside potential seems limited. Indeed, financial participants know that the 5-day Low target (whose today’s value is below the maximum coal switching level) will be difficult to reach. In these conditions, it is better to do nothing (which can explain the low intraday volatility of the past days) or bet on a rebound.