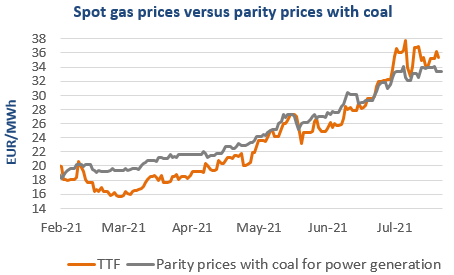

European gas prices weakened yesterday, pressured by rumors of an imminent US-German agreement on Nord Stream 2 and profit taking. The drop in parity prices with coal for power generation (both EUA and coal prices were down) also exerted downward pressure. On the pipeline supply side, Russian flows remained stable at 163 mm cm/day on average yesterday, with the Nord Stream 1 gas pipeline still shut for a 10-day planned maintenance that started on 13 July. Norwegian flows were down, averaging 323 mm cm/day, compared to 331 mm cm/day on Monday.

At the close, NBP ICE August 2021 prices dropped by 0.730 p/th day-on-day (-0.83%), to 87.650 p/th. TTF ICE August 2021 prices were down by 48 euro cents (-1.36%) at the close, to €35.165/MWh. On the far curve, TTF Cal 2022 prices were down by 15 euro cents (-0.60%), closing at €25.043/MWh.

Low stock levels, weak pipeline supply and strong Asia JKM prices remain supportive for European gas prices. Therefore, after yesterday’s drop, prices could rebound today. Technical resistances (€36.111/MWh on TTF August 2021 and €25.381/MWh on TTF Cal 2022) could however contribute to limit gains.

European gas prices weakened yesterday, pressured by rumors of an imminent US-German agreement on Nord Stream 2 and profit taking. The drop in parity prices with coal for power generation (both EUA and coal prices were down) also exerted downward pressure. On the pipeline supply side, Russian flows remained stable at 163 mm cm/day on average yesterday, with the Nord Stream 1 gas pipeline still shut for a 10-day planned maintenance that started on 13 July. Norwegian flows were down, averaging 323 mm cm/day, compared to 331 mm cm/day on Monday.

At the close, NBP ICE August 2021 prices dropped by 0.730 p/th day-on-day (-0.83%), to 87.650 p/th. TTF ICE August 2021 prices were down by 48 euro cents (-1.36%) at the close, to €35.165/MWh. On the far curve, TTF Cal 2022 prices were down by 15 euro cents (-0.60%), closing at €25.043/MWh.

Low stock levels, weak pipeline supply and strong Asia JKM prices remain supportive for European gas prices. Therefore, after yesterday’s drop, prices could rebound today. Technical resistances (€36.111/MWh on TTF August 2021 and €25.381/MWh on TTF Cal 2022) could however contribute to limit gains.