Sharp rise in interest rates and fall in the US dollar

Almost all the activity indicators published yesterday surprised on the upside, which supported risky assets and caused a sharp decline in the US dollar, in…

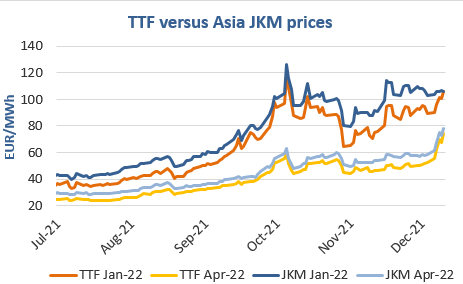

European gas prices increased strongly on Friday, supported by ongoing concerns on low Russian supply and weak gas stock levels. Asia JKM spot and month-ahead prices were rather stable (+0.30% on the spot, to €105.841/MWh; -0.08% for the January 2022 contract, to €106.232/MWh), but, as in Europe, the rise was stronger for Summer 2022 prices (+7.8% for the April 2022 contract). This is proof that the market expects the current competition between Europeans and Asians to attract LNG cargoes to extend into Summer 2022. On the spot pipeline supply side, Norwegian flows weakened on Friday, to 343 mm cm/day on average, compared to 351 mm cm/day on Thursday, due to an unplanned outage. Russian supply was almost stable, at 280 mm cm/day on average, compared to 279 mm cm/day on average on Thursday.

At the close, NBP ICE January 2022 prices increased by 12.690 p/th day-on-day (+4.95%), to 268.800 p/th. TTF ICE January 2022 prices were up by €5.33 (+5.31%) at the close, to €105.776/MWh. On the far curve, TTF Cal 2022 prices were up by €6.09 (+8.55%), closing at €77.306/MWh, with the spread against the coal parity price (€40.238/MWh, +3.14%) widening significantly.

TTF ICE January 2022 prices closed on Friday above the 5-day High. They are up again this morning, to €114.50/MWh, above Asia JKM prices Friday’s close. If Asian buyers do not outbid, TTF prices could weaken, thanks to the expected higher LNG supply. Otherwise, competition between the two zones could bring prices back to the records of early October. Whatever the scenario, Summer 2022 prices have a higher upside potential. Indeed, every day that passes (with weak Russian supply and low gas stocks) brings us closer to the situation where Europe will have to face a high injection demand next summer when Asia will face its (structural) summer peak in power consumption.