Diesel deficit growing in the Atlantic basin

According to the API industry survey, US crude stocks built by 5.2 mb w/w, while Cushing stocks dropped by 2.2 mb, lending support to the…

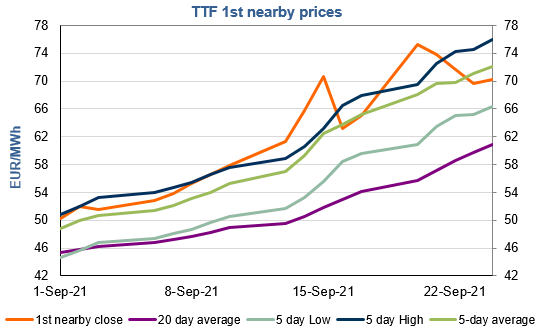

European gas spot and near curve prices rebounded overall on Friday, as the increase in pipeline supply was offset by the rise in Asia JKM prices (+2.45% on the spot, to €77.876/MWh, +2.79% for the November 2021 contract, to €80.090/MWh) and technical buying. Prices on the far curve increased even more strongly, supported by the rise in parity prices with coal for power generation (both coal and EUA prices were up).

On the pipeline supply side, Russian flows were almost stable on Friday, averaging 314 mm cm/day, compared to 313 mm cm/day on Thursday. Norwegian flows were significantly up, to 319 mm cm/day on average, compared to 289 mm cm/day on Thursday, as the technical incident on the Aasta Hansteen gas field has been settled.

At the close, NBP ICE October 2021 prices increased by 1.460 p/th day-on-day (+0.84%), to 175.950 p/th. TTF ICE October 2021 prices were up by 56 euro cents (+0.80%) at the close, to €70.240/MWh. On the far curve, TTF Cal 2022 prices were up by 159 euro cents (+3.72%), closing at €44.427/MWh, still significantly above the coal parity price (€37.692/MWh).

Weak stock levels, high Asia JKM prices (which should keep LNG supply to Europe at relatively low levels) and high coal prices remain supportive for European gas prices and additional increases are likely. Moreover, prices could also benefit from technical supports (€71.128/MWh on TTF October 2021 and €43.742/MWh on TTF Cal 2022).