Macro & Oil Report: Already less growth but still too much inflation

Macro & Oil Podcast #39 Despite the recovery in China, the IMF is expressing fears about global growth and the Fed is raising the prospect…

European gas prices extended gains yesterday as the sharp drop in Norwegian supply tightened gas balances even more. Indeed, due to an unplanned outage at the giant Troll field, Norwegian flows dropped to 293 mm cm/day on average yesterday, compared to 350 mm cm/day on Tuesday. Russian supply was stable, at 280 mm cm/day on average. The moderation in Asia JKM prices (+0.28% on the spot, to €104.701/MWh; -0.46% for the January 2022 contract, to €105.746/MWh) did not help to calm the bullish momentum because once again the rise was stronger for Summer 2022 prices which continued to reduce the spread against Q1 2022 prices.

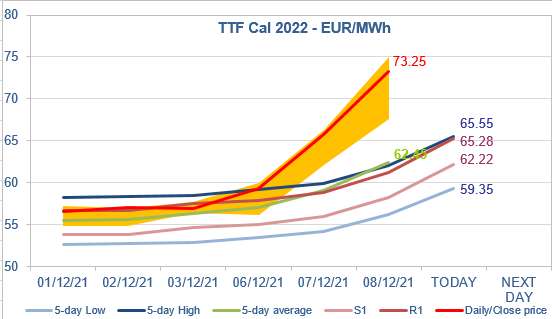

At the close, NBP ICE January 2022 prices increased by 16.350 p/th day-on-day (+6.70%), to 260.330 p/th. TTF ICE January 2022 prices were up by €5.62 (+5.86%) at the close, to €101.502/MWh. On the far curve, TTF Cal 2022 prices were up by €7.52 (+11.44%), closing at €73.254/MWh, with the spread against the coal parity price (€41.147/MWh, +4.01%) continuing to widen significantly.

TTF ICE January 2022 prices closed yesterday slightly above the 5-day High. They are down this morning, pressured by the strong rise in Norwegian flows (back to normal, to 350 mm cm/day on average) and by profit taking. As for TTF Cal 2022 prices, they continued to challenge the technical levels… having probably in sight their “fundamental” value, which could be close to Q1 2022 levels (currently at €99.09/MWh) if competition with Asia to attract LNG cargoes goes beyond Q1 2022 (because of low Russian supply and/or low gas stock levels which suggest strong injection demand next summer). Technical selling failed so far to calm the fundamental upward pressure, but it is still a possibility.