Backwardation is widening

The Brent contract change has caused the 1st-nearby to lose nearly $2/b due to the extremely sharp backwardation. It is trading below $89.5/b this morning. Backwardation…

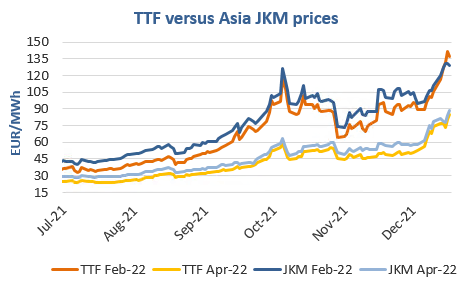

European gas prices weakened overall on Friday, pressured by the moderation in Asia JKM prices (-1.90% on the spot, to €118.982/MWh, -1.52% for the February 2022 contract, to €128.878/MWh) and a lower-than-expected drop in Russian supply: 281 mm cm/day on average, compared to 284 mm cm/day on Thursday. Moreover, this drop has been more than offset by the rise in Norwegian flows, which averaged 351 mm cm/day, compared to 342 mm cm/day on Thursday. Note also that the operator of the Nord Stream 2 pipeline announced that technical preparations of the infrastructure continue in anticipation of the commercial start, with the second string of the pipeline currently being filled with gas.

At the close, NBP ICE January 2022 prices dropped by 14.580 p/th day-on-day (-4.06%), to 344.900 p/th. TTF ICE January 2022 prices were down by €5.85 (-4.10%) at the close, to €136.913/MWh. On the far curve, TTF Cal 2022 prices were up by €1.82 (+1.99%), closing at €93.481/MWh.

TTF ICE January 2022 prices closed on Friday slightly above the 5-day High. They are up this morning, to €142.50/MWh, slightly above the 5-day High (€142.47/MWh). Given the moderation in Asia JKM prices, we expect this 5-day High to continue to oppose a resistance. But today, the market will probably take direction from the auctions of monthly transportation capacity as they should give an indication of the level of Russian gas flows for the month of January. A weak estimate could pull prices above the 5-day High. By contrast, a strong estimate could pull them down to the 5-day Low (€120.07/MWh).