European gas prices weakened

European gas prices weakened overall yesterday, pressured by the expected rise in temperatures from today. The drop in parity prices with coal for power generation…

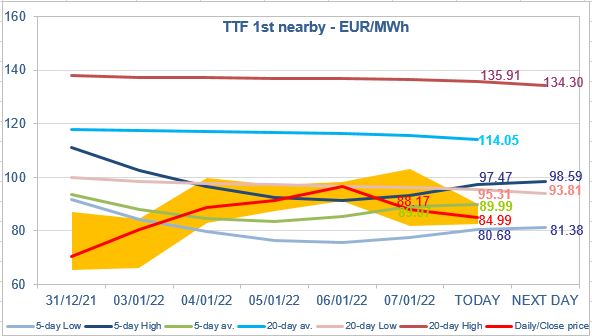

European gas prices weakened on Friday, apparently under pressure from the rebound in Norwegian supply (to 348 mm cm/day on average, compared to 341 mm cm/day on Thursday) and more generally the (slight) improvement in storage levels as net storage withdrawals are currently at historically low levels. On their side, Russian flows remained stable, at 185 mm cm/day on average. Asia JKM prices were slightly down (-0.80% on the spot, to €94.112/MWh; -0.95% for the February 2022 contract, to €101.983/MWh), widening their premium against European prices.

At the close, NBP ICE February 2022 prices dropped by 20.240 p/th day-on-day (-8.61%), to 214.960 p/th. TTF ICE February 2022 prices were down by €8.33 (-8.63%), closing at €88.174/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €3.01 (-5.93%), closing at €47.742/MWh.

We didn’t expect TTF ICE February 2022 prices to drop below the 20-day Low on Friday. They are down again this morning and seem heading towards the 5-day Low. From that level, they should rebound. This upcoming rebound is backed by the higher levels of Asia JKM prices (despite lower withdrawals, gas stocks remain too weak to allow Europe to do without LNG). Note that in Indonesia, the ban on coal exports is still in force; the energy minister said this morning the government is hoping to reach a decision on resuming coal shipments “in the coming days”.