European prices weakened

European gas prices weakened yesterday, both on the spot and the curve, pressured by the expected rise in temperatures above normal next week. The drop…

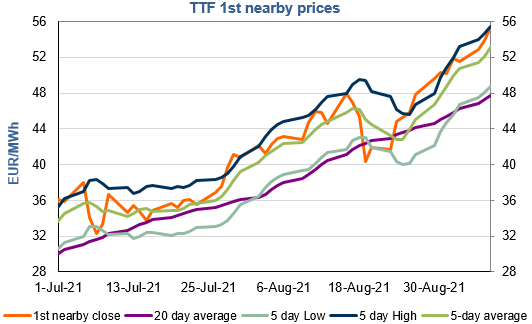

European gas prices maintained their bullish momentum yesterday as weak supply and low stock levels continued to raise concerns. Although Russian flows continued to rebound, averaging 296 mm cm/day (compared to 287 mm cm/day on Tuesday), thanks to the additional increase in flows through Poland to the Mallnow interconnection point, they are still below the levels of end August (313 mm cm/day). As expected, Norwegian flows dropped significantly, to 263 mm cm/day on average, compared to 282 mm cm/day on Tuesday, due to planned maintenance at Troll. The ongoing strength in Asia JKM prices (+0.03% for the October 2021 contract, to €53.870/MWh) and in parity prices with coal for power generation did not help calm the upward pressure.

Even the release of a news stating that Gazprom plans to start Nord Stream 2 on 1 October failed to exert a lasting downward pressure.

At the close, NBP ICE October 2021 prices increased by 3.220 p/th day-on-day (+2.36%), to 139.660 p/th. TTF ICE October 2021 prices were up by 138 euro cents (+2.56%) at the close, to €55.288/MWh. On the far curve, TTF Cal 2022 prices were up by 142 euro cents (+3.99%), closing at €36.960/MWh, increasing the spread against the coal parity price (€35.082/MWh).

Norwegian flows are recovering this morning (to 282 mm cm/day). This could limit the upward pressure on European gas prices today. Technical resistances (€56.530 /MWh on TTF October 2021 and €36.831/MWh on TTF Cal 2022) could also contribute to limit potential increases, particularly as the rise of TTF October 2021 prices above Asia JKM prices could lead some financial participants to start to reduce their buying interests.