Growth concerns outweigh inflation fears

The stock markets are back down this morning despite a rebound in the US markets at the end of the week, notably based on hopes for a…

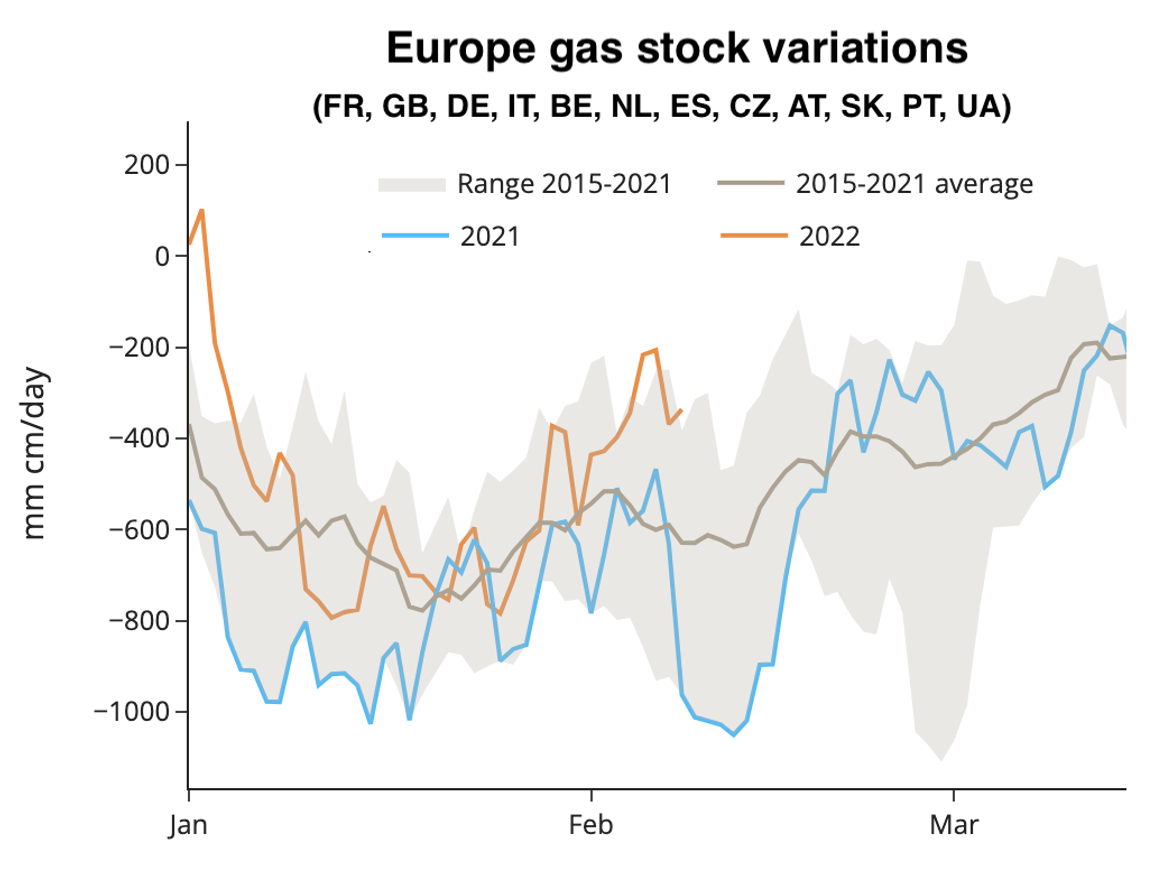

Globally mild and windy weather prospects for the coming two weeks as well as comfortable LNG supply continued to weigh on European gas prices on Wednesday in the absence of any significant development on the Russia-Ukraine-NATO conflict. TTF ICE March 2022 traded as low as €73/MWh intraday, their lowest level in two weeks. SUM 22 and WIN 22 prices posted the biggest losses, probably pressured by an improving storage picture thanks to limited withdrawals over the past two weeks (see chart).

Nominations for Russian gas imports at the Velke Kapusany entry point fell to 30 mm cm/day this morning, their lowest level since 23 January, probably in response to the drop in day-ahead prices across Europe yesterday. This could provide some support to prompt contracts today notably as heating demand is expected to rebound temporarily at the end of the week: UK gas demand is expected to be just below seasonal norms on Friday whereas it has dropped more than 20% below the five-year average over the past two weeks. But beyond this weekend, weather forecasts remain mild and windy across Western Europe, which could continue to limit the bullish potential in the short term. Otherwise, steady coal and EUA prices could continue to provide a fundamental floor on the downside, notably as coal supply remains scarce in both Atlantic and Pacific Basin amid governmental and technical constraints on production and exports.