European gas prices rebounded yesterday, supported by the increase in oil and Asia JKM prices and technical buying. The rise in parity prices with coal for power generation (both EUA and coal prices were up) also exerted upward pressure. On the pipeline supply side, Russian flows were almost stable at 162 mm cm/day on average yesterday (compared to 163 mm cm/day on Tuesday), as the Nord Stream 1 gas pipeline is still shut for a 10-day planned maintenance that started on 13 July. Norwegian flows were slightly down, averaging 320 mm cm/day, compared to 323 mm cm/day on Tuesday.

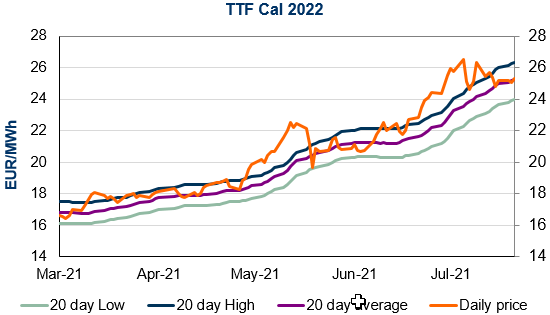

At the close, NBP ICE August 2021 prices increased by 2.030 p/th day-on-day (+2.32%), to 89.680 p/th. TTF ICE August 2021 prices were up by 78 euro cents (+2.23%) at the close, to €35.949/MWh. On the far curve, TTF Cal 2022 prices were up by 26 euro cents (1.03%), closing at €25.301/MWh.

Low stock levels, weak pipeline supply and strong Asia JKM prices remain supportive for European gas prices and additional gains are likely. However, profit taking and technical resistances (€36.668/MWh on TTF August 2021 and €25.511/MWh on TTF Cal 2022) could however contribute to limit gains today.

NWE spot baseload power prices weakened slightly yesterday, to €88.545/MWh on average for today delivery (compared to €92.695/MWh /MWh for Monday), as the impact of…

DOWNLOAD OUR SPECIAL REPORT EUAs broke all-time high : sustainable upward trend or temporary bullish run ? EUA prices have broken their all-time high of…

Brent prompt future contract approached 60 $/b on Tuesday, as Saudi OSPs unveiled the bullish Saudi outlook on prices while holding premiums to Asian customers…

Join EnergyScan

Get more analysis and data with our Premium subscription

European gas prices rebounded yesterday, supported by the increase in oil and Asia JKM prices and technical buying. The rise in parity prices with coal for power generation (both EUA and coal prices were up) also exerted upward pressure. On the pipeline supply side, Russian flows were almost stable at 162 mm cm/day on average yesterday (compared to 163 mm cm/day on Tuesday), as the Nord Stream 1 gas pipeline is still shut for a 10-day planned maintenance that started on 13 July. Norwegian flows were slightly down, averaging 320 mm cm/day, compared to 323 mm cm/day on Tuesday.

At the close, NBP ICE August 2021 prices increased by 2.030 p/th day-on-day (+2.32%), to 89.680 p/th. TTF ICE August 2021 prices were up by 78 euro cents (+2.23%) at the close, to €35.949/MWh. On the far curve, TTF Cal 2022 prices were up by 26 euro cents (1.03%), closing at €25.301/MWh.

Low stock levels, weak pipeline supply and strong Asia JKM prices remain supportive for European gas prices and additional gains are likely. However, profit taking and technical resistances (€36.668/MWh on TTF August 2021 and €25.511/MWh on TTF Cal 2022) could however contribute to limit gains today.