OPEC+ maintains its production policy for November

Crude prices rallied yesterday, as OPEC+ members met to decide their forward production policy for November. Dec-21 ICE Brent contract reached 81.6 $/b on early…

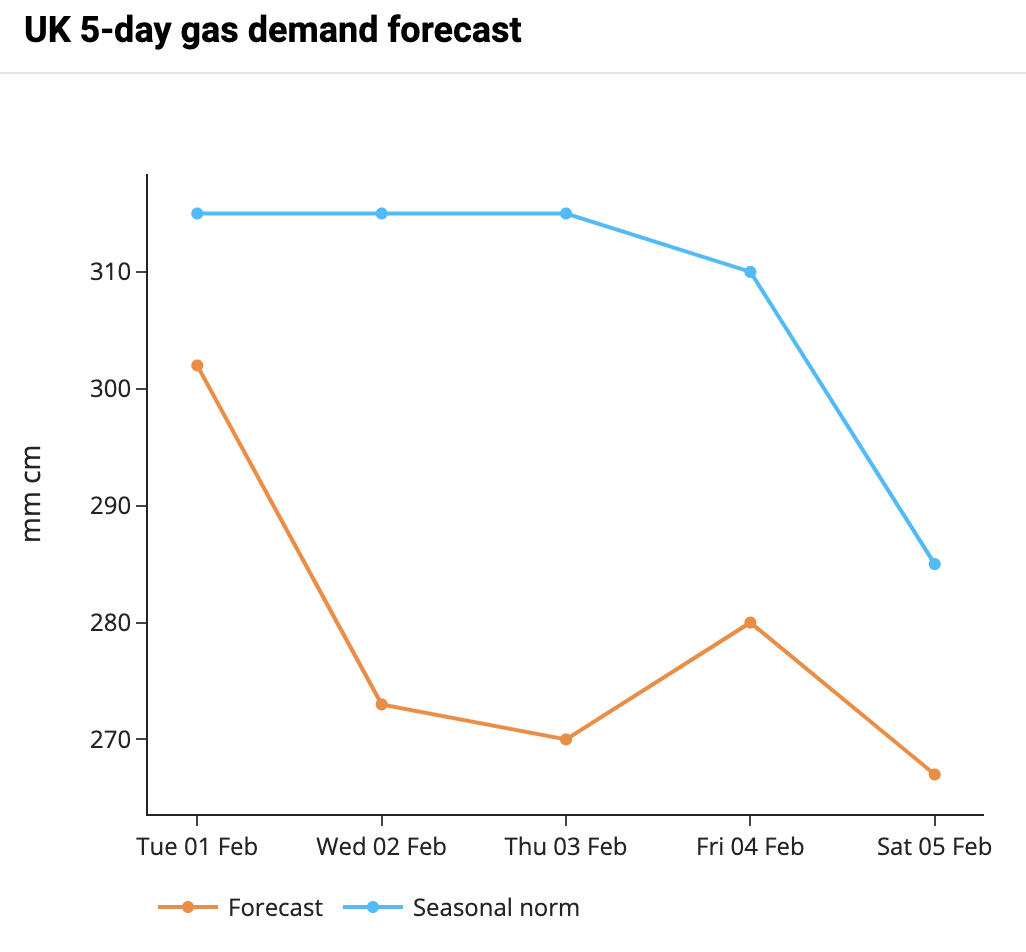

European gas prices eroded the risk premium built last week on Monday with biggest losses recorded on prompt and near-curve contracts as mild and very windy weather prospects for the coming days cut demand expectations. In the UK, gas demand is expected to drop by 14% below seasonal norms on Wednesday and Thursday according to National Grid (see chart). On the supply side, Equinor announced further delays in the resumption of the Hammerfest LNG export terminal (4.2 mmtpa capacity) which is now expected to restart on 17 May, 6 weeks later than previously announced.

Nominations for Russian gas imports at the Velke Kapusany are sharply up this morning to 80 mm cm/day, 30 mm cm/day higher day-on-day and corresponding to the capacity booked through the 5-year transit contract between Gazprom and GTSOU plus the monthly capacity booked for Feb-22 delivery. In addition, flows through Nordstream 1 are at capacity, up 10 mm cm/day and pushing total Russian gas imports to 243 mm cm/day, their highest level since late December. Combined with a very strong influx of LNG at EU import terminals, steady Norwegian production and weak demand prospects in the short term, this could continue to weigh and spot and near-curve contracts today.