Rally in Atlantic gasoline markets

Crude prices remained supported to 71.8 $/b for ICE Brent prompt futures. As the EIA weekly release showed a seasonally average week, with stock draws in crude…

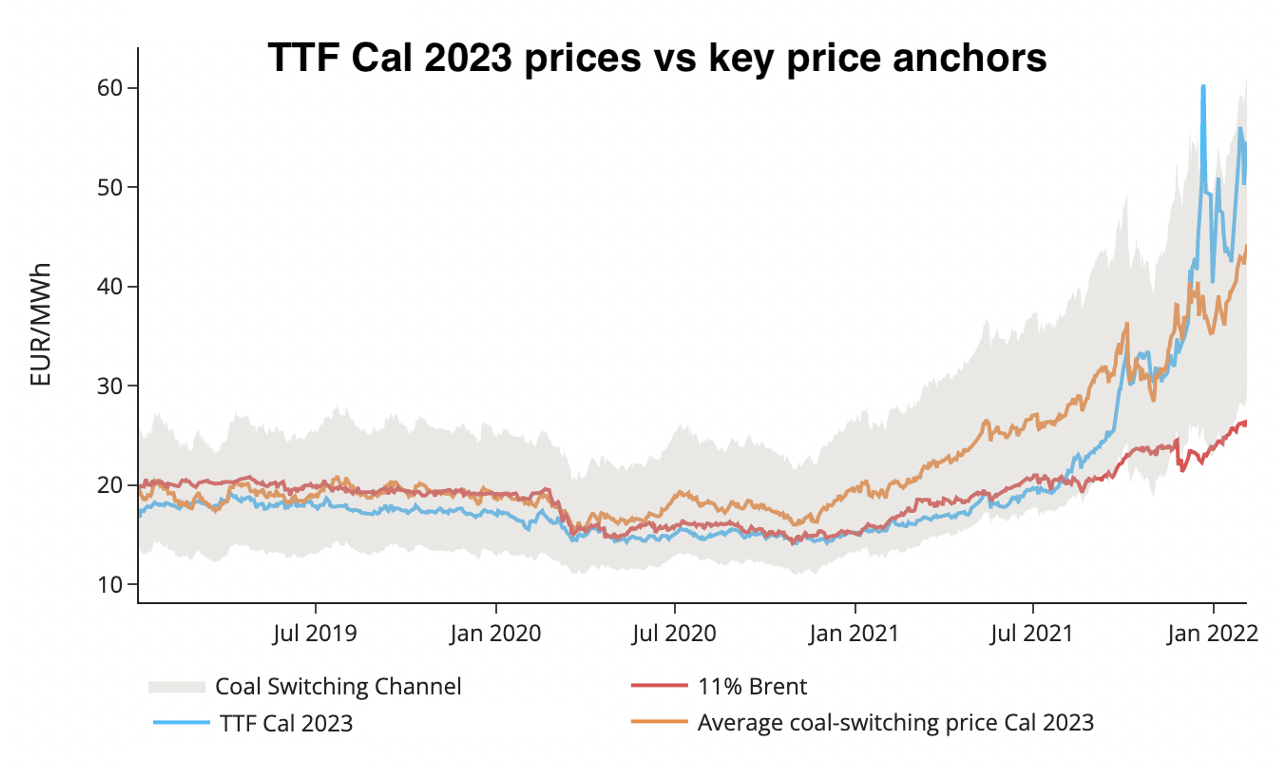

European gas prices ended the week on another bullish note on Friday, supported by a further drop in Russian gas flows through Ukraine and prospects of higher gas demand as temperatures were expected to normalize by mid-February. Strong Brent, oil and coal prices provided support to the far curve as well, with TTF Cal 23 prices remaining close to recent all-time highs towards the €55/MWh mark and still in the upper part of the coal-to-gas switching range.

Expectations of the return of above-average temperatures next week and a jump in nominations for Russian gas imports at the Velke Kapusany entry point to 80 mm cm/day for today dragged European gas prices down at the opening. The results of the quarterly transport capacity auction (at 12:00 CET) could have some impact as well, notably regarding capacity booked at delivery points for Russian gas (Mallnow and Velke Kapusany mainly). The outcome of Biden/Scholz in Washington and Putin/Macron in Moscow meetings over the Russia-Ukraine-NATO crisis will be closely watched by market players today who will look after concrete signs towards a de-escalation process in the Russian military build-up at the Ukrainian border.