European prices weakened on lower Asian prices

European gas prices weakened last Friday. Amid unchanged domestic fundamentals, the moderation in Asia JKM prices (-0.64%, to €108.740/MWh, on the spot; -8.16%, to €103.547/MWh,…

European gas prices were mixed on Friday as concerns on Russian deliveries were offset but ongoing strong LNG supply and weaker demand. The additional drop in coal prices (-3.49% for API2 1st nearby prices, -1.11% for Cal 2023 prices) exerted downward pressure. On the pipeline supply side, Russian flows were almost stable on Friday, averaging 223 mm cm/day, compared to 222 mm cm/day on Thursday. On their side, Norwegian flows increased slightly, to 304 mm cm/day on average, compared to 300 mm cm/day on Thursday.

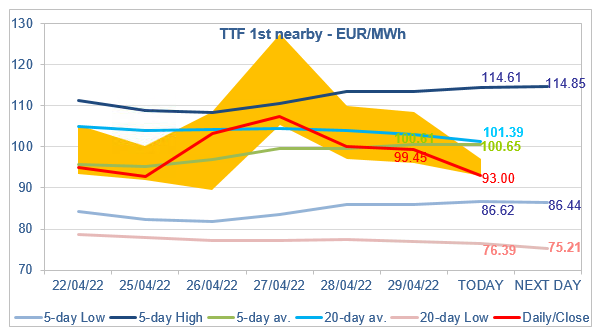

At the close, NBP ICE June 2022 prices increased by 3.770 p/th day-on-day (+2.36%), to 163.680 p/th. TTF ICE June 2022 prices were down by 39 euro cents (-0.39%), closing at €99.450/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 76 euro cents (-0.96%), closing at €78.482/MWh.

In Asia, JKM spot prices dropped by 1.76%, to €69.875/MWh; June 2022 prices dropped by 1.61%, to €79.404/MWh.

TTF ICE June 2022 prices resisted the downward pressure and managed to close around the 5-day average on Friday. They are down this morning, to 93.00/MWh at the time of writing. Yes, concerns on Russian deliveries remain a supporting factor but, given the level of Asia JKM prices and the level of the maximum coal switching level (88.47/MWh on Friday), we believe prices have more downside potential than upside in the very short term.