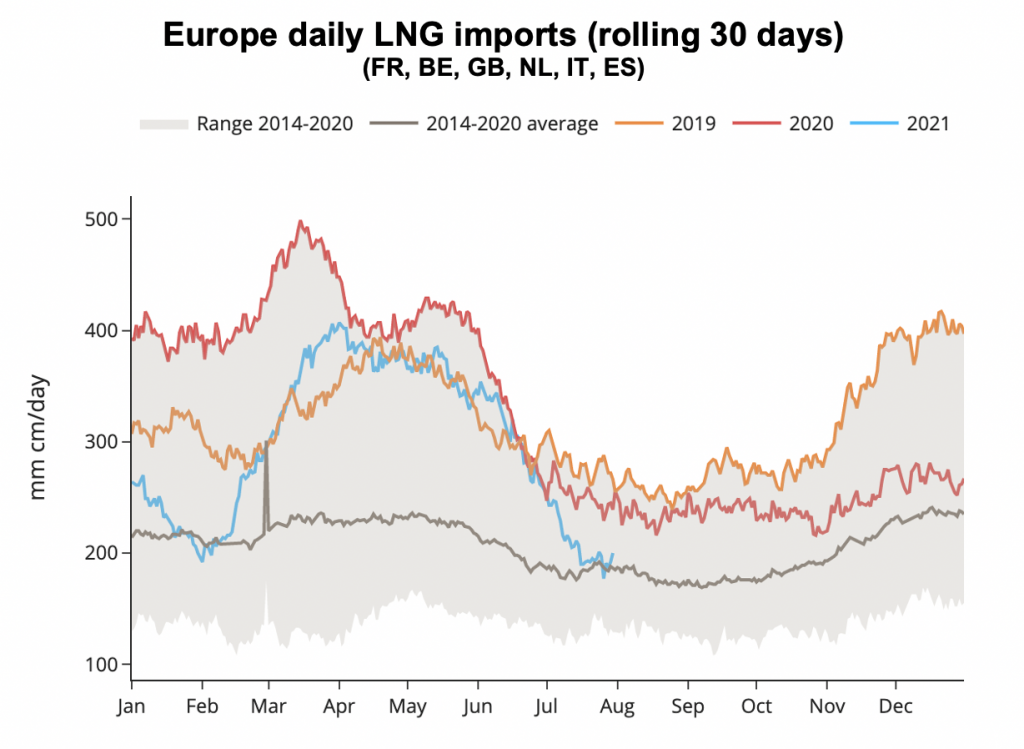

Natural gas prices continued to rise to record highs on Thursday with TTF prices trading above €40/MWh for the first time ever while JKM prices are approaching 8-year seasonal highs and are keeping European LNG supply tight (see below chart). Time spreads also traded in unchartered territories with the TTF Q4 21-Q1 22 spread nearing the €3/MWh mark and the WIN 21-SUM 22 spread settling at €15.60/MWh, highlighting the massive risk premium for the coming winter period. In the US, Tellurian’s Driftwood LNG project made a step closer to FID with the signature of a 3 mmtpa SPA with Shell for 10 years yesterday.

Volatility is likely to remain at elevated levels at European gas hubs today as fundamentals remain supportive but most contracts are trading in overbought territory. Overall, the bullish potential of EU gas prompt prices looks not exhausted regarding the upper bound of the coal-to-gas switching channel (see our TTF month-ahead prices vs key markers chart) and the willingness of Asian LNG buyers to maintain spot prices at high levels in the Pacific Basin to keep attracting cargoes so far.

The European power spot prices for today rebounded compared to Friday amid forecasts of lower temperatures and dropping wind output. Prices reached 50.35€/MWh on average…

Brent 1st-nearby is approaching $112/b this morning. Concerns about Russian oil flows have been compounded by a new episode of tension in the Middle East, with…

Natural gas prices continued to rise to record highs on Thursday with TTF prices trading above €40/MWh for the first time ever while JKM prices are approaching 8-year seasonal highs and are keeping European LNG supply tight (see below chart). Time spreads also traded in unchartered territories with the TTF Q4 21-Q1 22 spread nearing the €3/MWh mark and the WIN 21-SUM 22 spread settling at €15.60/MWh, highlighting the massive risk premium for the coming winter period. In the US, Tellurian’s Driftwood LNG project made a step closer to FID with the signature of a 3 mmtpa SPA with Shell for 10 years yesterday.

Volatility is likely to remain at elevated levels at European gas hubs today as fundamentals remain supportive but most contracts are trading in overbought territory. Overall, the bullish potential of EU gas prompt prices looks not exhausted regarding the upper bound of the coal-to-gas switching channel (see our TTF month-ahead prices vs key markers chart) and the willingness of Asian LNG buyers to maintain spot prices at high levels in the Pacific Basin to keep attracting cargoes so far.