2020 has been an astonishing period for energy markets. The historical demand shock implied by the Covid-19 outbreak was offset by a massive reduction in energy supply and upstream investments in a short timeframe, which triggered a quick rebalancing of global balances and a price recovery still ongoing in early 2021 despite some discrepancies among key commodities contracts. In Europe, power markets were also shaken by the combination of a plunge in France nuclear power generation and a new record high for EUA prices on the back of an historical agreement to further cut GHG emissions in 2030: the EU Green Deal.

Table of Contents

Join EnergyScan

Get more analysis and data with our Premium subscription

1. The Covid crisis will leave scars on economic activity

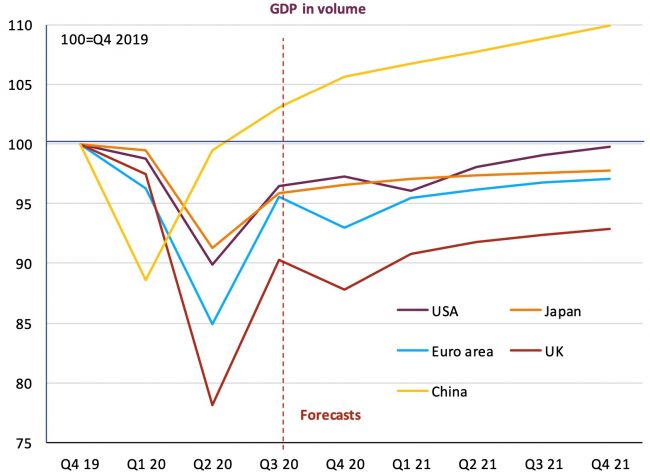

After an historical recession in 2020 (we expect a 3.8% contraction of world GDP this year), optimism is back regarding the economic activity outlook thanks to the impressively quick delivery of vaccines which already started to be inoculated to fragile populations in several countries. The success of these vaccination campaigns is of course a key driver of the expected economic recovery next year. But this rebound looks unequally distributed as China, which started recovering earlier, is projected to grow strongly, accounting for over 1/3 of world economic growth in 2021 according to the last OECD forecast.

Source: ENGIE EnergyScan

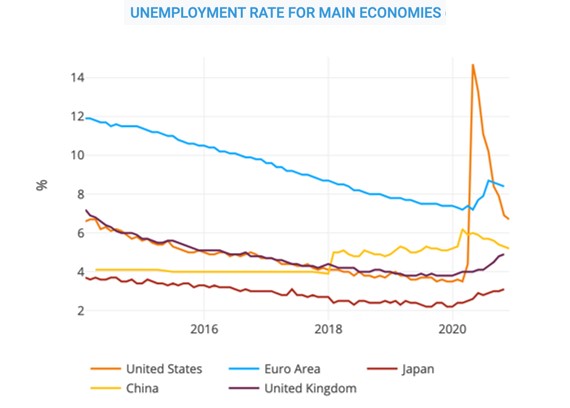

Indeed, whereas the growth momentum looks strong in China, the pandemic should continue to keep a lid on economic activity in the US and in Europe in 2021 after the disaster of 2020. It appears clearly that the size of the impact of the pandemic on health systems in 2020 is negatively correlated to the speed of the recovery in 2021. Finally, the Covid crisis will leave most countries with massive indebtedness and high unemployment rate at least until 2022.

Source: Trading Economics, ENGIE EnergyScan

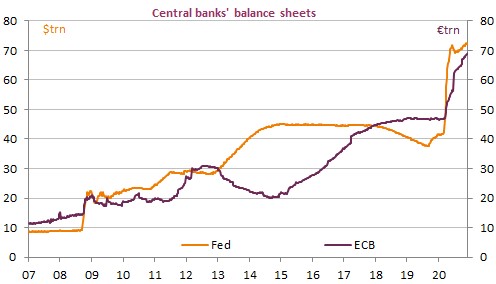

But government and central banks should remain particularly supportive after historical interventions in 2020 (see balance sheet chart below), taking advantage of the ultra-low level of interest rates that has reduced considerably the cost of additional debt.

Source: ENGIE EnergyScan

2. Energy prices have already recovered from the demand shock… except oil

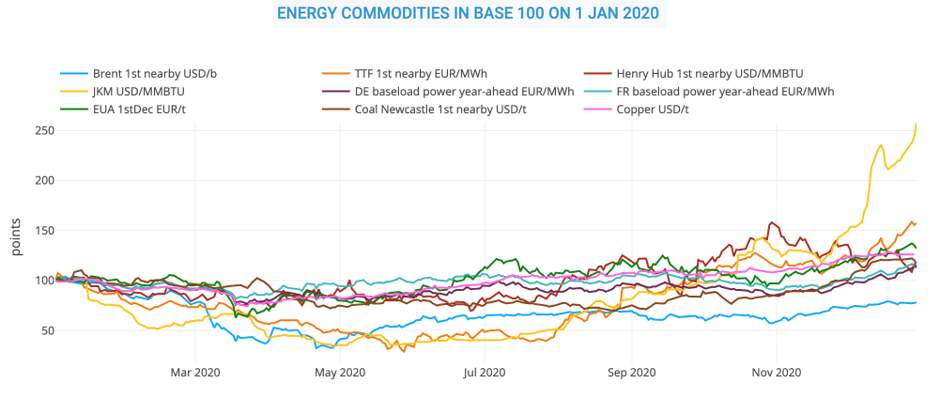

Thanks to a year-end rally, most energy prices will end 2020 at higher levels than January (and even twice higher for Asian LNG prices) before hitting record lows in Q2-20 as energy demand plunged on the back of multiple COVID-19 lockdowns across the globe which cut consumption from industrial, commercial and transport users.

Source: ICE, NYMEX, Investing, EEX

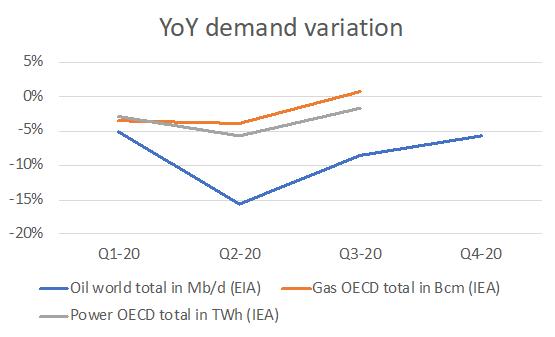

Source: IEA, EIA

Nevertheless, the impact was clearly less significant for power and natural gas demand compared to oil (see chart) and the recovery from Q3-20 is also slower for oil, notably due to prolonged travel restrictions across the globe. As a consequence, oil prices still remain 20% below their year-opening level in late December.

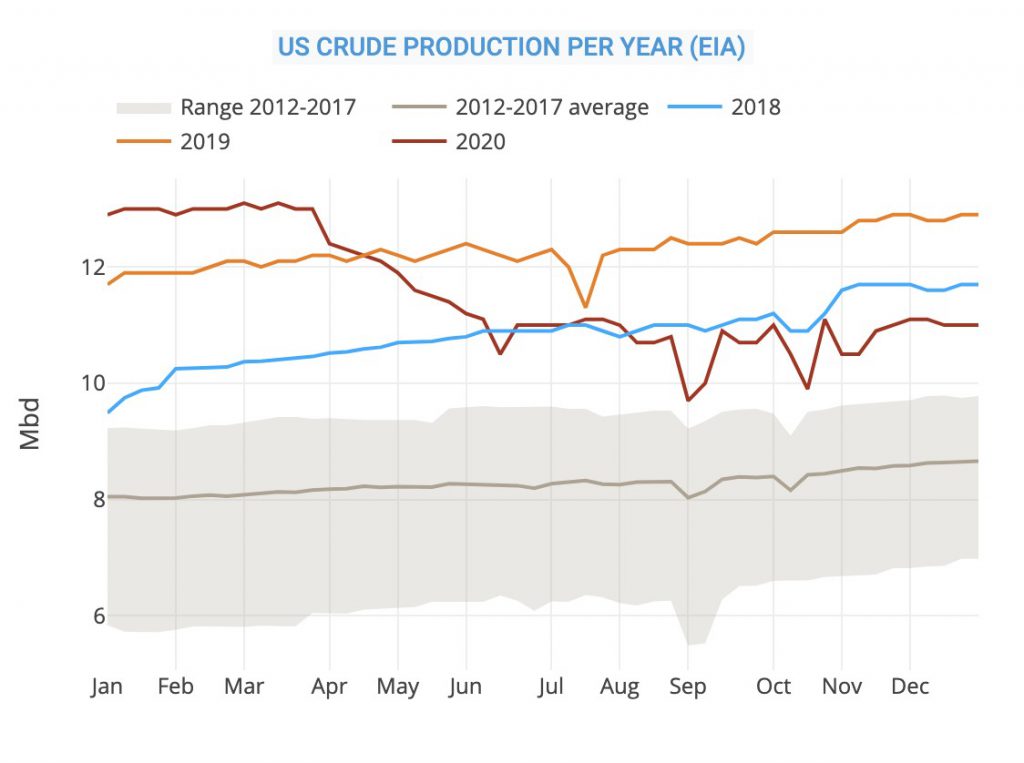

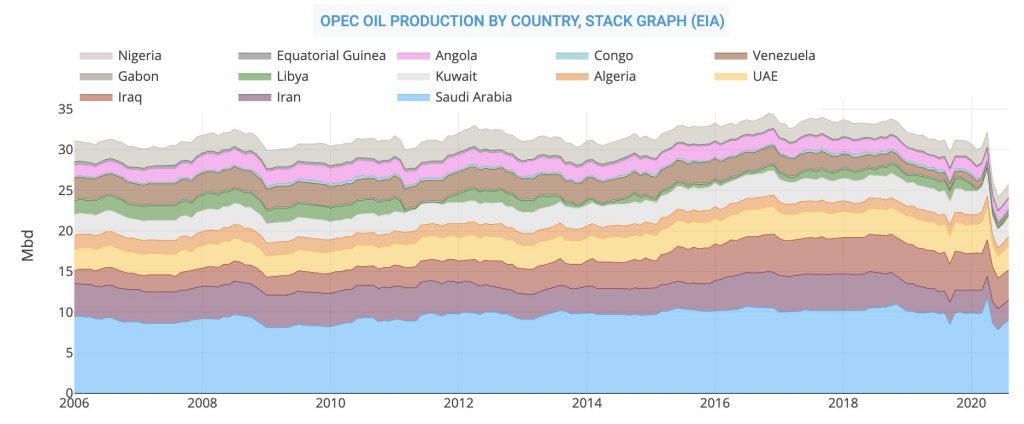

Massive oil and gas supply cuts also played a key role. On the oil side, OPEC producers were back into the fore with historical output cuts while US shale oil producers may be durably hit by the plunge in WTI prices (even into negative territory in May). Most US shale oil producers cut investments in 2020, which could lead to a tightening of the global oil balance as soon as 2021 if demand recovers to its pre-crisis level. Overall, we believe that oil prices could show a bigger upward potential than the rest of the energy complex next year, owing to their current recovery delay.

Source : EIA, ENGIE EnergyScan

Source : EIA, ENGIE EnergyScan

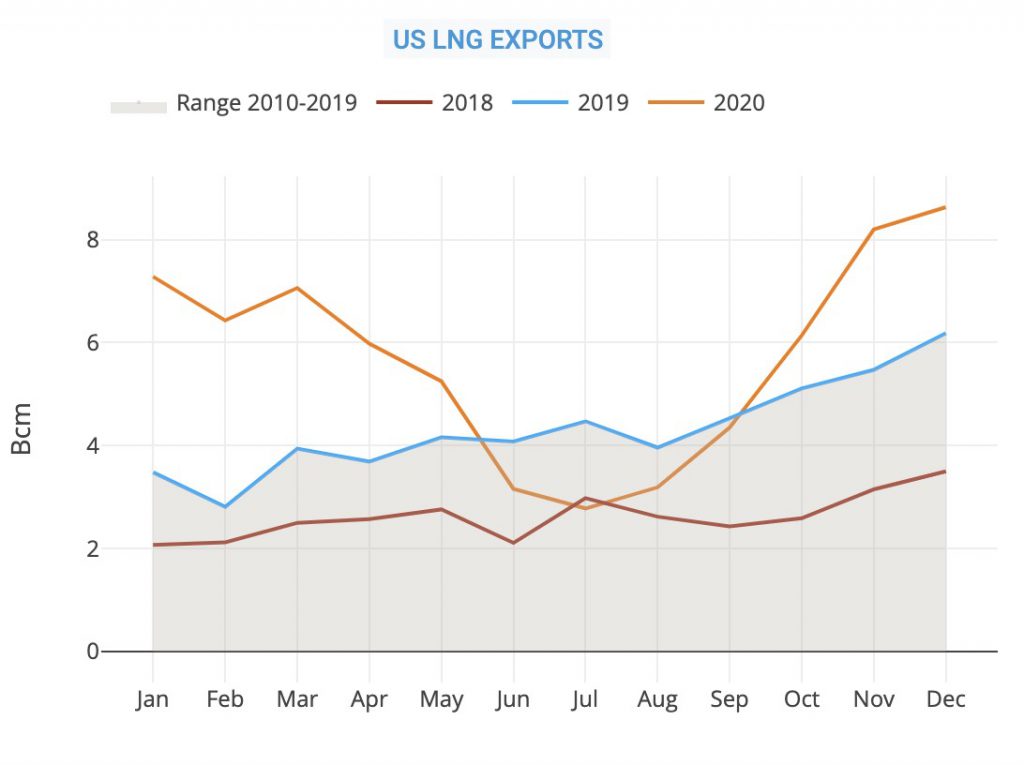

Dwindling gas prices in Europe and Asia triggered a massive drop in US LNG exports, consolidating the swing producer role of US LNG exporters in global gas markets. Nevertheless, Russia and Norway also cut pipeline exports to Europe significantly in 2020, avoiding a storage overhang last summer. A series of unplanned outages affecting LNG producers (hurricanes in the US Gulf, fire at the Hammerfest terminal in Norway, technical issues at Gorgon in Australia and Qatagas T4, etc…) in the second half of 2020 also played a key role in the recent explosion of Asian LNG prices.

Source : KPLER, ENGIE EnergyScan

Source : TSOs, ENGIE EnergyScan

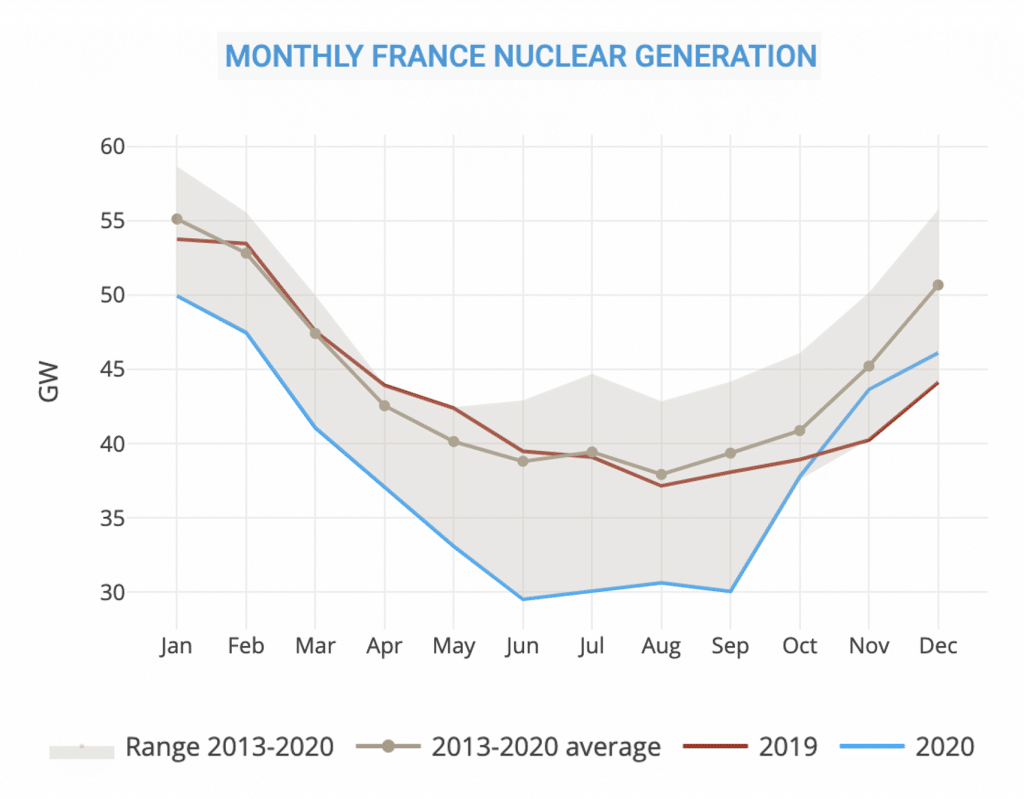

Finally, European power prices also rebounded strongly in Q4-20, following COVID19-driven nuclear supply cuts in France, stronger fuel prices and a rally in EUA prices (see next part).

Source : RTE, ENGIE EnergyScan

3. The EU green deal pushed EUA prices to new highs

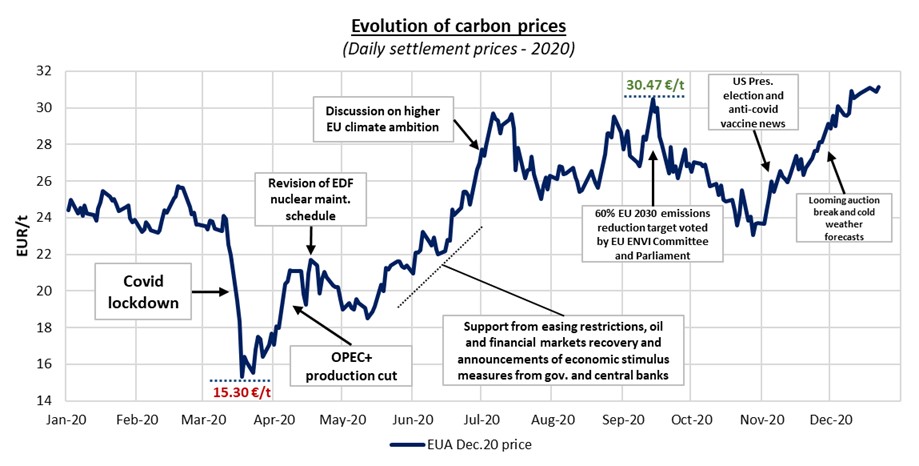

Despite a record drop in CO2 emissions this year due to the recession (up to 12% yoy in Europe according to a recent study), European Union Allowance prices hit new record highs in December 2020 after several weeks of bullishness, supported by a combination of optimism over the economic recovery, stronger thermal power generation to cope with cold weather across Europe, delays in auctions and free allocations for 2021 and a widely-awaited new CO2 emission reduction target agreed by EU leaders from 40% currently to 55% below 1990 levels by 2030 as part of the EU Climate Law proposed by the European Commission.

Source : ICE, ENGIE EnergyScan

Nevertheless, in the medium term EUA prices could continue to observe a high volatility with the startup of the Phase IV in 2021 as market players wait for the European Commission proposals on the EU ETS review scheduled in June 2021. Brexit developments and a potential worsening of the health situation regarding the Covid-19 pandemic could also inject some volatility in early 2021. Meanwhile, the auction supply will remain heavy with the Market Stability Reserve absorbing part of the surplus generated by the Covid-19 crisis only from September 2021. A slow economic recovery might have a long-term impact as well on the demand for allowances from industrial and power sectors.

4. The pipeline of new LNG trains has dried up

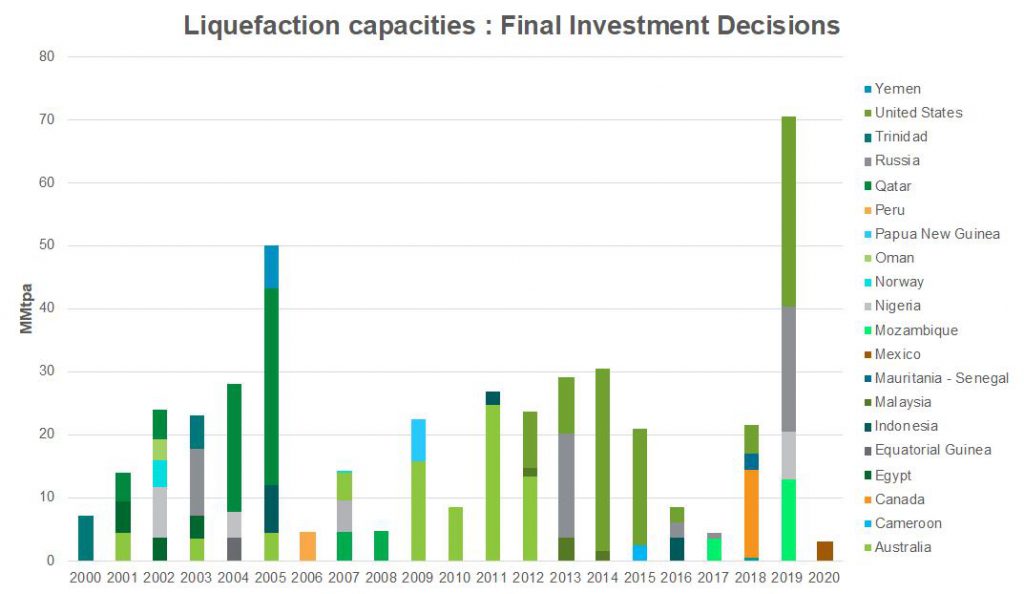

After a record high in 2019 at 70 MMtpa, investments in new liquefaction capacities plunged to a record low in 2020, with only one Final Investment Decision sanctioned by the Energía Costa Azul LNG project in Mexico for a nameplate capacity of 3.25 MMtpa. The collapse of gas prices in Europe and Asia played a key role, but as seen before, US LNG shut-ins during summer 20 may have also freighted investors.

Source : IHS Markit

2021 could see a rebound in LNG FIDs as Asian LNG prices jumped to a six-year high in December due to a combination of steady industrial demand in China, cold weather, tight shipping capacity and multiple supply issues. But a tightening of global LNG markets cannot be excluded in the short term if the economic recovery continues and keeps gas demand growth at a steady level in northeast Asia, especially in China. Nuclear and coal phase out plans in Europe could also keep gas-for-power demand steady. On the supply side, we should not see any significant additional liquefaction capacity before 2024, with a second wave of new liquefaction capacities mostly from the US and Qatar. But most additional trains should come after 2025.

5. Europe is ahead of a growing peak power supply shortage issue

With ageing flexible thermal power plants and a growing intermittent renewable capacity, European power markets are already facing a structural rise in price volatility. But the plunge in French nuclear output emphasized the trend and triggered several short-term peak power supply shortage issues in the UK in 2020, notably as France used to be a net power exporter to this country. Balancing power prices hit record highs in the UK several times in 2020 despite the setup of capacity mechanism, notably in March and December due to a combination of cold weather, tight interconnection capacities and low renewable power generation. Belgium was also affected by power supply issues due to a lack of flexible capacity in December with balancing prices topping €2250/MWh.

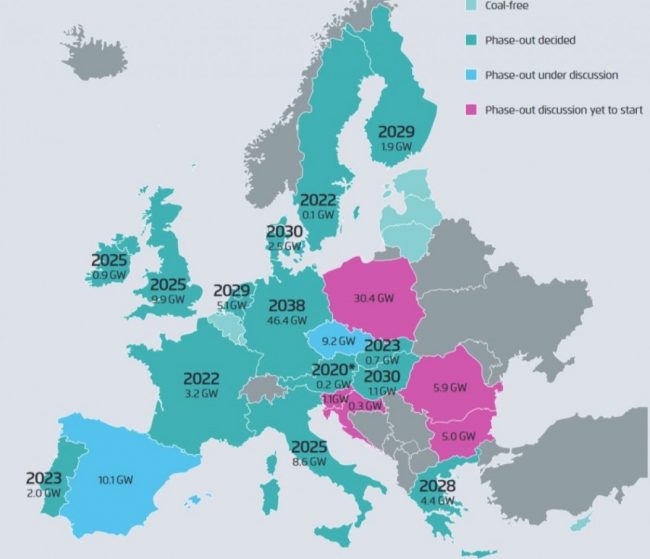

Several national power TSOs in Europe warned that supply margins are tight for this winter despite the second wave of covid restrictions dampening power demand as the French nuclear availability is expected to drop significantly from February. Nuclear and coal phase out plans in Germany, Netherlands, France, Italy, Belgium and the UK (see map) could emphasize the trend despite a growing renewable power supply. Indeed, the recent 55% CO2 emission target could imply a quicker-than-expected reduction of thermal power capacity in certain countries notably Germany where nuclear power generation is already expected to end by 2023 and still represents 8 GW of available capacity in late 2020.