Massive Fed balance sheet reduction in sight

The FOMC Meeting Minutes unveiled details over a significant balance sheet reduction set to start as soon as next month with bond sales up to $95bn…

Profit taking in the equity markets yesterday, particularly in the wake of the anti-Covid measures taken in the UK, reminded everyone that the fact that the Omicron variant is not very aggressive in the first place would not prevent negative economic consequences in the short term. The fact that it is also highly contagious may also lead to an initial overload in hospitals even if intensive care units are spared. The announcement of the default of the Chinese property developers Evergrande and Kaisa has also created some concern, without having a big impact for the moment.

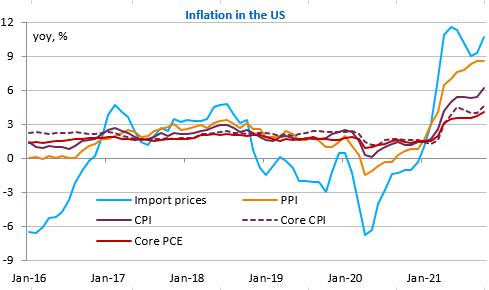

The release of US jobless claims data at the lowest since 1969 started a return to the markets’ main concern: inflation and the expected tightening of Fed policy. US November inflation figures will be released today and are expected to be close to 7%.

The consensus is already high (6.8%). The risks of unpleasant surprises therefore seem limited. The University of Michigan’s consumer survey should also serve as a reminder that inflation threatens to cripple the recovery through its impact on household purchasing power.