Mixed picture for crude prices

After a strong start, Brent prices turned slightly negative on Tuesday afternoon and touched an intraday low at $104.53/b, pressured by a stronger USD following…

The publication of very good activity data in the US reinforced the rise in bond yields (the US “10 year” has recovered 20bp in 4 sessions) and pushed the dollar to its highest level since July 2020. Retail sales rose by 1.7% in October and industrial production rose by 1.6%. The NAHB housing market index rebounded by 3 points in November, returning to its levels of the beginning of the year. According to the Atlanta Fed’s estimates, GDP growth could rebound to 8.7% in Q4. For completeness, we should add that the yoy growth rate in import prices reached 10.7% in October, which will continue to push up the inflation rate.

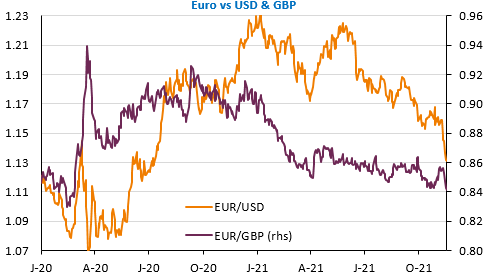

Conversely, the euro continues to fall: markets seem to agree with the ECB President’s speech that inflation will fall rapidly in 2022. Moreover, the epidemic recovery is clouding short-term growth forecasts. The euro’s effective exchange rate is at its lowest since May 2020 and the EUR/USD exchange rate fell below 1.13 overnight. The EUR/GBP exchange rate also broke through 0.84 for the first time since February 2020. The acceleration of inflation to 4.2% yoy in October in the UK clearly increases the probability of a BoE rate hike in December.

Today, the final Eurozone inflation figures for October and the US construction figures for October. The main reports expected this week have already been released.