2021 Energy Markets Outlook

The EnergyScan team held its quarterly webinar covering key trends and events on energy markets. In this webinar, our experts addressed the following topics, with…

European gas prices increased again yesterday, as concerns on supply scarcity continued to fuel the strong uptrend. The announcement by the operator of the Nord Stream 2 pipeline that it had started filling one of the two legs with gas for tests only provided a moderate and temporary downward impact. The rise in Asia JKM prices and in parity prices with coal for power generation (both coal and EUA prices were up) provided additional support.

Note that Russian supply dropped to 254 mm cm/day on average yesterday, compared to 263 mm cm/day on Friday, due to the additional drop in Yamal flows to the Mallnow entry point. Norwegian flows were almost stable, averaging 346 mm cm/day, compared to 344 mm cm/day on Friday.

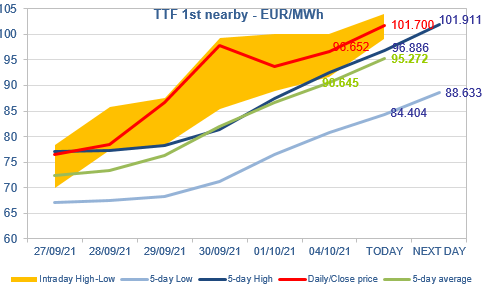

At the close, NBP ICE November 2021 prices increased by 4.610 p/th day-on-day (+1.91%), to 245.870 p/th. TTF ICE November 2021 prices were up by €3.03 (+3.23%) at the close, to €96.652/MWh. On the far curve, TTF Cal 2022 prices were up by €2.76 (+4.88%), closing at €59.223/MWh, and widening the spread against the coal parity price (€44.221/MWh, +3.84%).

The start of filling of the Nord Stream 2 pipeline could have been the fundamental element the market was waiting for to erase the risk premium on Russian gas. But the market seems to be asking more. TTF ICE November 2021 prices are up again this morning, well above the 5-day High for today (which is known, at €96.886/MWh), but close to the 5-day High for tomorrow (unknown and partly depending on today’s close price, and currently at €101.911/MWh). This is the fine tuning financial participants are proceeding: buy at a level not too high to be able to sell back the following day with a profit.