ICE Brent prompt contracts declined to 74 $/b, from 76.5 $/b between Tuesday and today, as sources within OPEC+ mentioned that a deal was within reach between Saudi Arabia and the UAE. The UAE could potentially be allowed to pump 3.61 mb/d during the extension of the current deal, between April and December 2022. Following that, Iraq also mentioned that they would potentially re-negotiate their quotas, in light of the recent moves from the UAE. Details of the deal have yet to be confirmed, and we could potentially have to wait for a more formal OPEC+ meeting to have clear commitments from OPEC+ members (no meetings for August are scheduled yet). We believe the deal will likely affect production post-2021, and the UAE will return to the 2021 production plan suggested by Saudi Arabia and Russia, hereby ramping up production by 0.4 mb/d monthly increments.

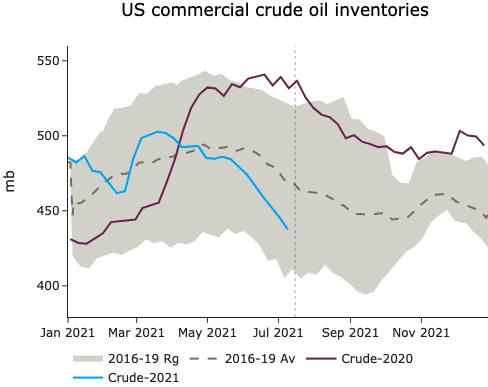

On the US side, a slightly bearish EIA weekly report showed continued draws in crude stocks (7.9 mb) while builds across gasoline, distillate and jet fuel stocks were respectively recorded at 1 mb, 3.7 mb, and -0.7 mb. Draws in the US crude inventories were helped by a decline in net crude imports of 1 mb/d w/w. Domestic crude production crept higher, at 11.4 mb/d. US WTI time spreads declined significantly, with a combination of rolling pressure from financial players and the prospects of higher net imports, boosted by a high WTI/Brent spread, which incentivized West African cargoes to flow West.

This was to be expected. Some European countries are too dependent on oil from Russia to declare an embargo overnight. This is particularly true of Austria and…

Prices rebounded in most European gas markets yesterday, supported by tight pipeline supply and technical rebound. Russian supply was almost stable, averaging 247 mm cm/day,…

Join EnergyScan

Get more analysis and data with our Premium subscription