Oil above $100/b, European gas climbs, and power prices turn negative as geopolitics, weak confidence, and supply risks reshape energy markets.

Energy markets remain dominated by geopolitical risk as the near‑closure of the Strait of Hormuz continues to reverberate across oil, gas, power, and carbon markets. Brent prices are holding above $100/b, while European gas prices rise amid low storage levels and supply constraints. At the same time, power markets face renewed negative pricing driven by strong renewable generation.

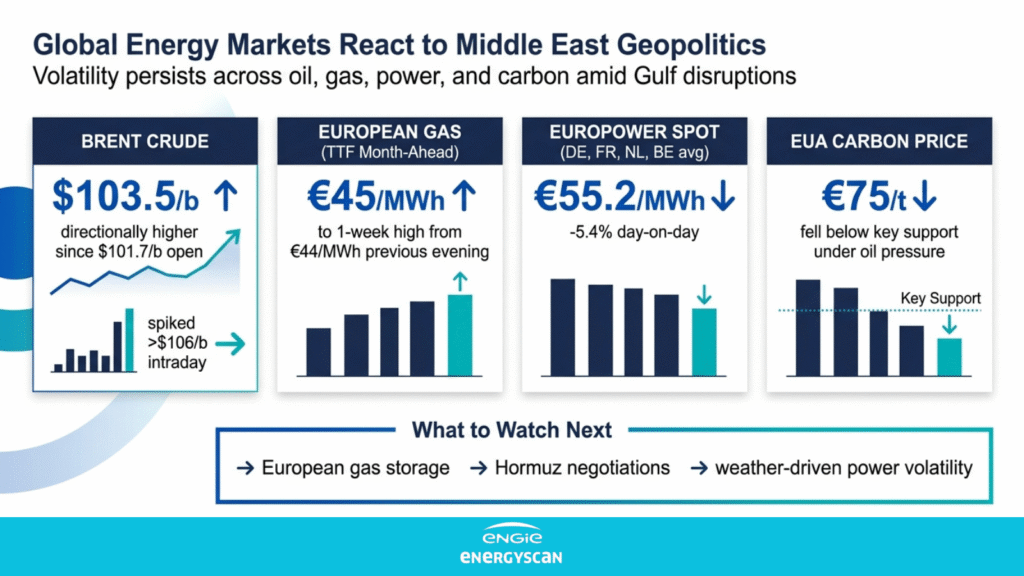

Oil Markets: Physical Disruption Keeps Brent Above $100/b

Oil prices remain firmly supported as the situation around the Strait of Hormuz continues to deteriorate. Brent settled above $100/b and is trading around $103–104/b, with markets increasingly pricing a prolonged disruption rather than a short‑lived shock.

The main driver is physical disruption to maritime flows. Iranian forces have fired on commercial vessels and seized at least two ships, while US naval forces have intercepted and turned back tankers linked to Iran. Since the start of the US blockade, 31 ships have reportedly turned around while only 34 have managed to transit the strait. Iran has made clear it will not reopen Hormuz unless the blockade is lifted, effectively extending the near‑closure into a second month.

Diplomatic signals remain inconsistent. While the US extended the ceasefire announced on April 7 without a fixed end date, planned talks in Islamabad were cancelled after Iran declined to attend. Unconfirmed reports of explosions in Iran briefly pushed Brent more than 4% higher intraday, highlighting the highly headline‑driven nature of oil price formation.

Beyond geopolitics, fundamentals are also lending support. US inventories declined across major refined product categories, while global demand for US barrels lifted total oil and fuel exports to a new record. In California, diesel prices have climbed well above $7/gal as refinery closures, record‑low distillate stocks, and weak refinery runs sharply reduce local supply.

Gas Markets: Europe Tightens as Storage Remains Low

European gas prices continue to track oil higher, supported by ongoing tensions in the Middle East and domestic supply constraints. The TTF month‑ahead contract moved above €44/MWh and reached a one‑week high above €45/MWh, marked by significant intraday volatility.

Supply‑side risks persist. A brief outage at Norway’s Aasta Hansteen field provided short‑term support, while the Troll field remains under planned maintenance until May 7. Forward curves are increasingly backwardated, reflecting low storage levels across Europe.

Average EU gas storage fullness currently stands just above 30%, around six percentage points below last year at the same time. Although LNG send‑outs have remained broadly stable, the average net injection rate since the start of the month is still lagging last year’s pace. Against this backdrop, the TTF Q3‑26 / Q1‑27 spread has widened toward €1.70/MWh, its highest level since mid‑April.

In response, the European Commission signaled openness to further easing storage‑filling targets, potentially lowering the requirement to 75% after already cutting it from 90% to 80%.

Power Markets: Negative Prices Return

Power markets across Central Western Europe are again experiencing strong downward pressure. Spot prices for delivery today averaged €55.2/MWh across Germany, France, the Netherlands, and Belgium, down more than 5% from the previous day. French prices fell to particularly low levels around €20.8/MWh.

The primary drivers are strong renewable output and seasonal temperatures. High wind generation in Germany, combined with exceptionally strong solar production, is pushing prices lower across the region. In France and Spain, robust solar generation is dragging prices toward deep negative territory, near ‑€50/MWh, despite weaker wind support during morning hours.

Looking ahead, slightly cooler temperatures are expected next week in northern markets, while solar output is forecast to remain strong.

Carbon: EUAs Behave as a Macro Asset

Carbon prices continued to decline, with EUAs falling below the €75/t support level. Despite rising oil prices, sentiment remains weighed down by expectations of weaker industrial activity. Recent positioning data shows net short positions being reduced, largely via short covering rather than renewed long conviction.

European forward power prices moved higher despite weaker carbon, supported by gas prices. German Cal‑27 continued to rise, while France underperformed, widening the spread between the two markets.

Key takeaways

- Hormuz disruption remains the dominant market driver, keeping Brent firmly above $100/b.

- European gas prices are supported by geopolitics and low storage, despite steady LNG flows.

- Power markets face renewed negative pricing due to exceptionally strong solar and wind generation.

Conclusion

Through mid-April, European gas prices eased not because risks disappeared, but because they stopped intensifying over the period. However, the rebound seen at the start of the following week is a reminder that the market remains highly reactive to new signals and that any easing in the risk premium can quickly reverse.

keywords

- Brent crude oil

- Strait of Hormuz

- European gas prices

- TTF gas

- Power prices Europe

- Carbon EUA

- Energy market volatility