Curve prices up after a volatile session

NWE spot baseload power prices were up yesterday, to €118.879/MWh on average for today delivery (compared to €112.274/MW for Wednesday), supported by forecasts of lower…

Mixed news from China: Covid cases in Beijing are back to a record high… at 99. The number seems ridiculously low, but the trend is worrying, especially in the context of the “zero cases” policy. But on the other hand, the President seemed to open the door to at least a partial lifting of the trade sanctions put in place by his predecessor.

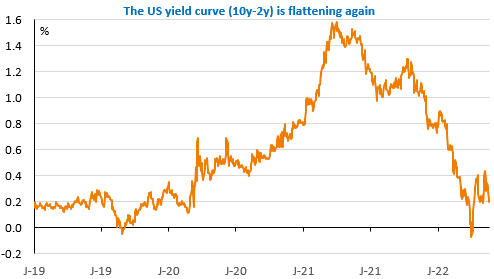

Will this be enough to break the downward momentum of the US equity markets, which recorded their 7th consecutive decline last week? We will come back to this in our Macro & Oil Weekly Report. Fears of recession due to monetary tightening, the war in Ukraine and the grip of the pandemic on the Chinese economy continue to drive the markets. The US yield curve, which had temporarily re-steepened, is flattening again as markets still expect a sharp Fed rate hike but believe that a very sharp economic slowdown will be the result. In this context, the decline of the US dollar could be premature: the EUR/USD exchange rate has crossed 1.06. Certainly the euro is benefiting from the ECB’s rate hike expectations, but risk aversion should remain strong.

This week, we will be watching the business surveys, starting with the IFO in Germany, as well as several key reports in the United States on household consumption, investment and the trade balance, as well as the minutes of the last Fed meeting. Let’s not forget the Davos meeting that was postponed.