EUAs faded despite firmer gas prices

The European power spot prices eased yesterday, weighed by forecasts of milder temperatures and stronger wind output. The day-ahead prices averaged 193.13€/MWh in Germany, France,…

Three days without a new case of Covid in Shanghai. According to the rules established by the local authorities, this should open the way to a gradual lifting of the restrictive measures imposed for weeks and thus to a resumption of activity. As we suspected yesterday, the markets were not too badly affected by the very poor activity figures in April to turn to these hopes of recovery. At least that is the trend in the Asian markets. The figures published early this morning should reinforce this positive trend as they show a drop in unemployment in both France and the UK. Long term yields are rising with the US 10 year at 2.92% and the EUR/USD exchange rate is showing a clear rebound above 1.0470.

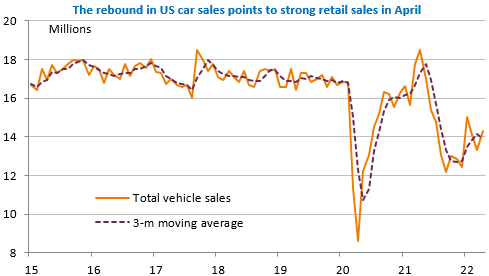

Revised and detailed Q1 Eurozone GDP growth figures will be released this morning (0.2%), but the main focus is on US retail sales and industrial production figures as well as the NAHB construction sector index. Retail sales are expected to rise sharply after the rebound in car sales, but we would be tempted to say that this does not matter for monetary policy: if they are indeed strong, it will reinforce the need to slow growth to calm inflation. If they are weak, it will be attributed to the impact of inflation on purchasing power… Watch out for the NAHB index as rising rates should start to seriously dampen the housing market. For the rest of the week, you can refer to the Macro & Oil Weekly Report.