Surging gas prices triggered sell-off in EU ETS

The European power spot prices pursued their ascend yesterday, driven further up by the soaring gas prices despite forecasts of slightly weaker power demand. The…

European gas prices maintained their uptrend overall yesterday, supported by the additional rise in coal prices: +3.20% for API2 1st nearby prices; +3.04% for Cal 2023 prices. (More details are available in the Gas & Coal Weekly Report published yesterday.)

Norwegian flows weakened significantly yesterday, to 321 mm cm/day on average, compared to 337 mm cm/day on Wednesday, due to planned maintenance works. On their side, Russian flows remained stable, averaging 260 mm cm/day.

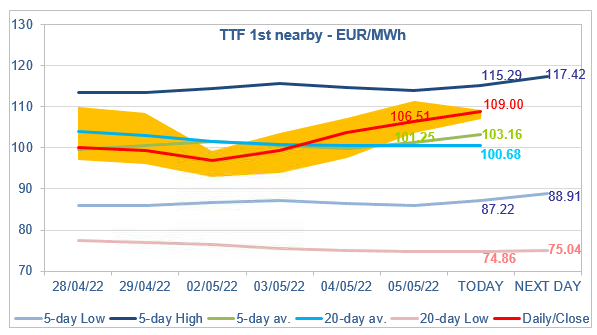

At the close, NBP ICE June 2022 prices increased by 7.030 p/th (+4.42%), to 166.230 p/th. TTF ICE June 2022 prices were up by €2.69 (+2.59%), closing at €106.508/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €2.38 (+2.87%), closing at €85.368/MWh.

In Asia, JKM spot prices increased by 2.03%, to €76.489/MWh; June 2022 prices increased by 1.21%, to €78.166/MWh.

The additional rise in coal prices pulled the maximum coal switching level to 102.37/MWh yesterday (up from 99.44/MWh on Wednesday), which continued to offer upside potential to TTF ICE June 2022 prices. Prices are up again this morning. The 5-day average, which is close to the maximum coal switching level, is now a strong support level. For the bulls, the 5-day High (115.29/MWh for today) seems to be an achievable target in the very short term.