EU Parliament finally agreed on common position for ETS revision

The European power spot prices reverted yesterday, the French and German day-ahead prices decreasing on forecasts of higher nuclear availability and wind output while prices…

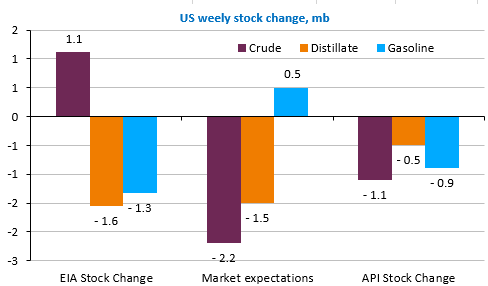

The oil market has been quite volatile since yesterday: the price of Brent 1st-nearby exceeded $96/b before plunging to $91/b and then rising to $94/b this morning. Despite the (supposed) easing of geopolitical tensions, prices rose again yesterday against the backdrop of a short-term imbalance between dynamic demand and rigid supply. The surprise rise in US crude oil inventories did not have a negative impact as it was mainly due to a temporary drop in refinery activity in Texas caused by the cold snap. More details here.

It was then statements by the French Foreign Minister that the West, but also China and Russia, had reached an agreement on Iranian oil and by the head of the Iranian negotiators that “an agreement is closer than ever” that led to the price plunge. According to Jean-Yves Le Drian, if Iran accepts the terms of the agreement, it could be signed in the coming days.

But this was without counting on the not very reassuring news coming from Ukraine, which reports incursions of Russian troops into its territory, while the Biden Administration believes that there is nothing on the ground to indicate that Russia has committed to a withdrawal of its troops. Uncertainty therefore, but all this seems to confirm that if the price of Brent crude does not reach $100/b before Iranian oil returns to the market, the likelihood of it doing so afterwards will be significantly reduced.