Risky assets extend their rally

Whatever the reason, the same story repeats again and again: each downward correction on financial markets is seen as a buying opportunity by many. This…

European gas prices ended the session with minor moves on Thursday despite a bullish start on the back of a drop in nominations for Russian gas imports through Ukraine at the Velke Kapusany entry point. Favorable weather continued to exert bearish sentiment on the prompt while seaborne coal prices corrected downwards as the Chinese NDRC announced at a conference on 9 Feb a series of measures to improve production and cap prices at local mines in order to prevent domestic prices from rising further.

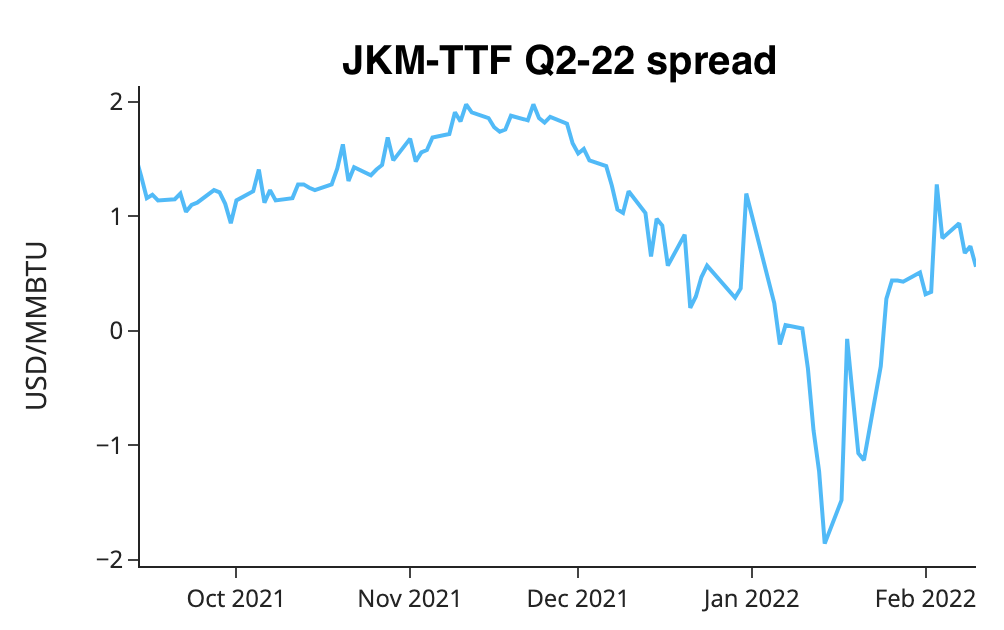

An upward revision in temperature forecasts for next week could continue to weigh on prompt contracts at European gas hubs today as temperatures are now expected to be up to 5-6 Celsius degrees above seasonal norms in northwestern Europe mid next week. On the supply side, nominations for Russian gas imports at Velke are slightly down again this morning but the LNG delivery schedule remains particularly busy in western Europe for the coming two weeks, which should keep European gas systems relatively comfortable. JKM-TTF spreads for Q2-22 delivery drifted lower over the past few days (see chart) and this could indicate that the current LNG wave to Europe could be prolonged beyond March if the downward trend continues. Market players should keep an eye on comments and developments surrounding Russian military exercises in Belarus and naval drills in the Black Sea that began yesterday with UK’s Prime Minister Boris Johnson stating that the Russia-NATO clash was facing “its most dangerous moment” in the next few days.